Abstract

Despite a recent surge of interest, the subject of pricing in general and value-based pricing in particular has received little academic investigation. Yet, pricing has a huge impact on financial results, both in absolute terms and relative to other instruments of the marketing mix. The objective of this paper is to present a comprehensive framework for pricing decisions which considers all relevant dimensions and elements for profitable and sustainable pricing decisions. The theoretical framework is useful for guiding new product pricing decisions as well as for implementing price-repositioning strategies for existing products. The practical application of this framework is illustrated by a case study involving the pricing decision for a major product launch at a global chemical company.

D 2003 Elsevier Inc. All rights reserved.

Keywords: Value-based pricing; Cost volume profit; Economic value analysis

1. Introduction

Pricing is an important and largely neglected tool in industrial marketing—on average, a 5% price increase leads to a 22% improvement in operating profits—far more than other tools of operational management. On the other hand, the subject of pricing has received far less attention than other aspects of marketing, from both practitioners as well as academic scholars. In this paper, an integrative framework for pricing decisions is presented. Based on economic value analysis, cost volume profit (CVP) analysis, and competitive analysis, it is shown how to determine and implement profitable pricing decisions. Several examples illustrate how to use the pricing methodology presented in this paper to improve firm profitability.

2. Pricing in today’s theory and practice

Pricing has largely been neglected by managers. Despite all laments of intensified price competition and the perceived difficulty of raising prices, empirical re- search by McKinsey & Company has shown that less

than 15% of companies do any systematic research on pricing (Clancy & Shulman, 1993).

Pricing has received little academic investigation. Not only managers, but also academics, have shown little interest in the subject of pricing: Publications on this subject are not anywhere as numerous as publications on other classical marketing instruments such as product, promotion, and distribution. Even marketing scholars have devoted only little effort to pricing theory and practice: An empirical study revealed that less than 2% of all articles published in major marketing journals cover the subject of pricing (Malhorta, 1996).

Consumers show little interest in prices of goods pur- chased. Managers have a general tendency to believe that price is an important issue for customers. Research, however, has shown that customers are frequently unaware of prices paid and that price is one of the least important purchase criteria for them.

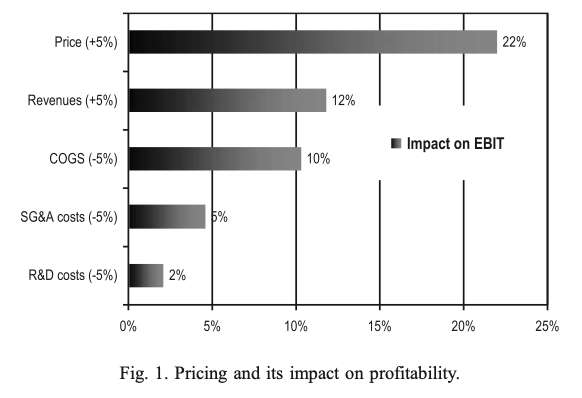

Impact of price on profitability is high. Finally, the impact of even small increases in price on profitability by far exceeds the impact of other levers of operational management as shown in Fig. 1 (based on a sample of Fortune 500 companies).

A 5% increase in average selling price increases earnings before interest and taxes (EBIT) by 22% on average, compared with the increase of 12% and 10% for a corresponding increase in turnover and reduction in costs of goods sold, respectively.

Given the high impact of pricing on profitability, why has the subject attracted so little interest in management practice?

According to the author’s experience, managers seem to have fallen victim to two erroneous beliefs. First, managers seem to believe that there is nowhere else conflict is so strong as in the field of pricing. The dominant assumption is that what is gained by the firm is lost by the customer and vice versa, and that pricing is, in the end, a zero-sum game. Second, managers generally do not seem to believe in their ability to significantly influence their industry’s pricing structure. A common managerial lament is the following: ‘‘In our industry, prices are mostly dictated by the market. Therefore, we focus on costs and volumes.’’

In this paper, it is shown that these assumptions and their underlying logic are incorrect and harmful to a company’s profitability. It seems that executives perceive it as far easier to strip the product of some features, to cut advertising budgets, to reduce costs rather than to imple- ment and communicate price increases.

In conclusion, it seems that managers suffer from systematic misconceptions when confronted with pricing decisions. Two of the most common misconceptions will be analyzed in the following sections.

3. Exploring common myths in pricing

3.1. A myth: premium prices and high market share are incompatible

Implicitly, most managers seem to have taken to heart one of marketing’s first, apparently obvious, and outdated

lessons: The traditional advice of marketing literature is to set prices low at the introduction stage of new products if the objective is to gain market share rapidly (Lamb, Hair, & McDaniel, 2000). ‘‘Penetration pricing,’’ that is, low prices, is recommended if the objective is to build market share, whereas ‘‘price skimming,’’ that is, high prices, is recom- mended if the objective is to increase (short-term) profits (Lamb et al., 2000). Marketing executives have been reluc- tant to price new products significantly above current price levels, fearing that this might put them at a competitive disadvantage in the quest for market leadership.

The implicit assumption that high prices and high market share are incompatible is simply incorrect. In a variety of industries, from software to pharmaceuticals, specialty chem- icals to cars, aircraft to apparel, it is quite common for the premium price brand to also be a market share leader. Let us analyze the U.S. pharmaceutical industry for this purpose.

The pharmaceutical industry is an interesting research setting, where a high drive for innovation and high pressures on cost containment both coexist. Pharmaceutical marketing is, in its essence, industrial marketing. Almost 80% of employed Americans are now covered by either a health maintenance organization (HMO), a preferred provider organization, and a point-of-service plan, that is, managed care. About 90% of HMOs now use formularies (Pharma- ceutical Research and Manufacturers of America, 2001). A formulary is a list of prescription drugs approved for insurance coverage. As drugs are selected principally on the bases of therapeutic value, side effects, and cost, pharmaceutical marketing consists to a large degree of convincing managed care organizations to put a specific drug on formularies, that is, on the list of drugs eligible for reimbursement.

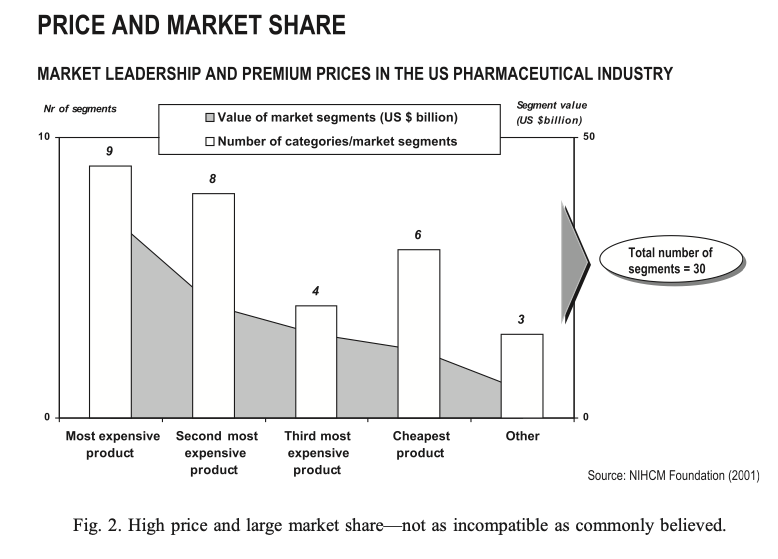

The U.S. pharmaceutical industry is divided into 30 market segments such as antibiotics, diabetes drugs, cho- lesterol lowering drugs, etc. (National Institute for Health Care Management, 2001). The absolute price level of the market share leader was analyzed for each market segment. Contrary to expectations, it was found that in nine segments, the most expensive drug was at the same time also the drug with the largest market share. The second most expensive product was a market share leader in eight segments. By contrast, the cheapest product had the largest market share in six, and only 20%, of all segments (see Fig. 2).

Traditionally, most managers would hesitate to associate market share leadership with a high-price strategy; the belief is that a premium price strategy is best suited for small, niche markets.

High market share and high prices can be achieved if prices truly reflect high customer value. This aspect will be further discussed in the next section. Before doing so, one key question needs to be answered: Are customers really as price sensitive as most managers believe? This question is particularly relevant given that, in empirical surveys, mar- keting managers frequently mention intensified price com- petition as the main challenge, ahead of issues such as product differentiation and new product launches (Simon, 1999).

3.2. Are customers really as price sensitive as commonly believed?

A second, closely related misconception concerns the price knowledge and sensitivity of customers. Both factors have been extensively tested in numerous studies. In this section, the most salient results are summarized.

Avila, Dodds, Chapman, Mann, and Wahlers (1993)

investigated the importance of price for industrial goods in a survey involving purchasing and sales managers of 200 companies. They found that purchasing managers ranked product attributes as the most important criteria, then service attributes, and finally, price as the least important criterion. Sales managers, by contrast, ranked price much higher in what they perceived to be the most important purchasing criteria of their customers, indicating how weak their understanding of the critical purchasing criteria of their customers was.

Price awareness has been researched extensively in the consumer goods industry. Given that industrial and high- tech firms frequently have companies in the consumer goods industry as their direct customers, the price sensitivity in consumer goods markets is at least of indirect relevance also for industrial companies. Dickson and Sawyer (1990) examined the extent to which supermarket shoppers were aware of prices paid. They found that 50% could not correctly name the price of the item they had just placed in their shopping cart, and that more than half of the shoppers who purchased an item on sale were unaware that the price was reduced.

Hoch, Dreze, and Purk (1994) examined the effects of category-wide price increases in a chain of 86 supermarkets involving 5000 products. A price increase of 10% led to a volume decrease of less than 3%, suggesting that customers show little sensitivity to price increases.

In conclusion, it seems that managers, as price setters, have a general tendency to overestimate the importance of price for actual and potential customers.

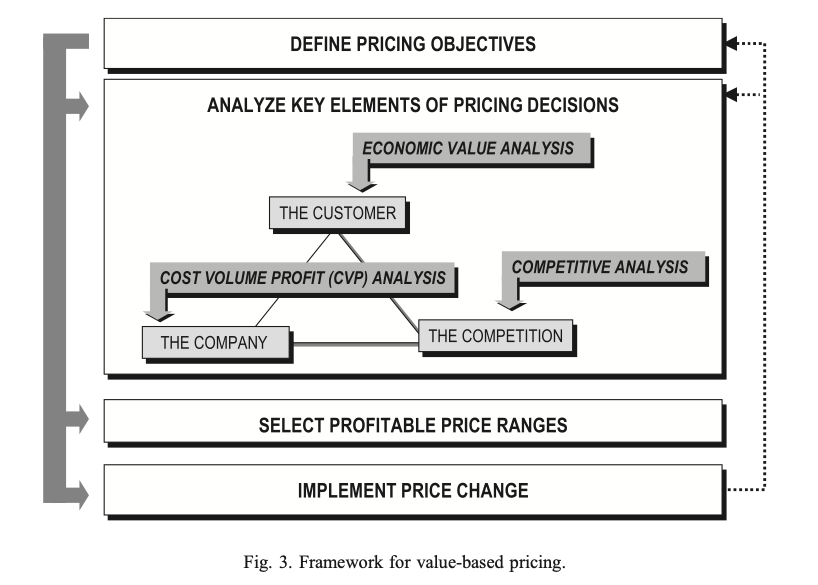

4. A framework for pricing

The following framework for effective pricing decisions is proposed. The starting point is a clear definition of the objectives of the pricing process. Subsequently, the three critical elements of all strategic decisions are considered, that is, the company perspective, the customer perspective, and the competitive perspective. Each perspective is then related to one specific tool to capture the implications for pricing purposes. As a result, profitable prices and ranges of prices can be selected in a third step. Finally, ways to implement price changes are examined. Shipley and Jobber (2001) suggest to view pricing as a continuous process: Changes in environmental conditions, in marketing strategy, and in customer needs can require to change selected elements of the pricing process, which in turn can lead to a modification of the prices adopted.

4.1. Define pricing objectives

Shipley and Jobber (2001) propose that the determina- tion of the objectives of the pricing process is the starting point of pricing strategies. The objectives of the pricing process are a direct result of a company’s overall strategy. A company may pursue a growth strategy of rapidly increasing market penetration and market share. This will require, at least in the short term, the adoption of a different pricing strategy than the pursuit of a strategy aimed at increasing profits over time. A company may also decide to sell certain products at and below the cost to attract customers to stores, to cross-sell other more profit- able products, to bundle the product with other products, to preempt competitive entry into certain markets and seg- ments, to sell out a declining product line, to transmit signals to the market, and so on.

Pricing objectives are bound to vary by type of product and over time, even within a company and business unit. Although the objective of the pricing process is to determine a pricing strategy, which will be a basis for profitable decisions in the medium and long term, pricing strategies are always context-specific and thus bound to change.

Even global companies, such as DuPont, rarely adopt a truly global pricing strategy, as the specific elements of profitable pricing decisions depend upon local market con- ditions and country-specific marketing objectives. A profit- able pricing strategy in one country might be a marketing blunder in another country.

4.2. Analyze key elements of pricing decisions

It is most useful to view pricing decisions in light of the strategic triangle originally developed by Ohmae (1982). For each of the three dimensions—company, customers, and competition—the author proposes to use specific tools to guide profitable pricing decisions. CVP analysis should be used to capture the company-internal perspective, compet- itive analysis to gain insight on trends in competitive strategies, and economic value analysis to understand sour- ces of value for customers. Each of these instruments will be discussed in turn in the next sections. All pricing decisions should take into account the frame- work developed in Fig. 3. This framework suggests question such as, ‘‘How do prices affect volumes and profits?’’

‘‘How will competitors react to different pricing strategies?’’ and finally, ‘‘What is the economic value of the product and service in question to different customer segments?’’ Once these questions are answered, pricing decisions can be built on a well-founded basis rather than following the accoun- tant’s cry for a minimum margin and the sales manager’s desire for competitive price levels.

Consider the case of Schering-Plough’s Claritin in the oral-cold drug market. The product carried a price premi- um of over 200% over existing drugs and established itself as the category leader only 2 years after launch. This was possible only after having gained a profound under- standing of the sources of value of the product to customers.

Traditionally, marketing executives would have been reluctant to price a new product significantly above exist- ing price levels, especially if the goal is to gain market leadership. A profound understanding of the sources of value for customers helps to avoid one common error in pricing decisions: pricing truly innovative products far too low.

In this section, managers will be provided with the tools that will help to implement profitable pricing policies and to increase long-term profits of their business line and company. It is proposed to implement pricing decisions only after having gained insight into each of the following points:

– economic value analysis: the understanding of the sources of economic value of a product to different clusters of customers;

– CVP analysis: the understanding of the implications of price and volume changes on company profitability; and

– competitive analysis: the understanding of trends in competitive pricing, product offerings, and strategies.

4.2.1. Economic value analysis

The concept of customer value2 is frequently used in practice, but rarely defined and quantified. HP, for example, states that one of its key objectives is to ‘‘continually improve the value of the products and services offered to customers.’’ Reichheld, a prolific author on customer loy- alty, says that ‘‘. . .the only way a business can retain customer and employee loyalty is by delivering superior value’’ (Reichheld, 1996).

This statement is, in its essence, correct. The author believes, however, that while many companies have capa- bilities to design and launch superior products, most of them fail utterly when it comes to quantifying the value of these products to actual and potential customers. In the author’s experience, it is at least as important to create customer value by innovative products and services, as it is important to quantify and to communicate the value of these products to customers through pricing and marketing activities.

Economic value analysis is a tool designed to compre- hend and to quantify the sources of value of a given product for a group of potential customers. It is clear that it is not always possible to set the price only in function of the value of a product; however, without knowing a product’s value, profitable pricing decisions cannot be made.

The concept of economic (or customer) value is being interpreted in two different ways. According to Simpson, Siguaw, and Baker (2001); Ulaga and Chacour (2001); Walter, Ritter, and Gemuenden (2001), and Zeithaml (1988), customer value is the difference between perceived benefits and sacrifices. In microeconomic terms, customer value is seen here as the difference between the consumer’s willingness to pay and the actual price paid, which is equal to the ‘‘consumer surplus,’’ the excess value retained by the consumer.

A second line of thought defines customer value in a broader way: Forbis and Mehta (1983, 2000); Golub and Henry (2000); Nagle and Holden (1999), and Priem (2000) define customer value as the maximum amount a customer would pay to obtain a given product, that is, the price that would leave the customer indifferent between the purchase and foregoing the purchase. Customer value in this sense is equal to the microeconomic concept of a customer’s ‘‘reservation price’’ and the use value of goods.

The difficulty of the former approach of defining economic value lies in the fact that price is part of the definition: Each time alternative approaches to pricing strategy are considered, economic value for the customer will necessarily change. As the objective here is the conceptual exploration of alternative pricing strategies, a definition of value is required, which is independent from price. The following definition is thus proposed: A

product’s economic value is the price of the customer’s best alternative—reference value—plus the value of what- ever differentiates the offering from the alternative— differentiation value (Nagle & Holden, 1999).

In this definition, reference is thus made to the received value of customers—the value customer actually experience through specific product – customer interactions—and not to customers’ desired value—the value customers want from products and services and their providers (Flint & Woodruff, 2001).

The proposed definition further satisfies key elements which Ulaga and Chacour (2001) require from customer value measurement approaches, namely, the requirement of (a) identification of benefits and sacrifices, (b) distinction between customer segments and use situations, (c) multi- informant approach, and finally, (d) the comparison with alternative suppliers’ offerings. Elements (a) and (d) are inherent to the definition, while (b) and (c) will be discussed in the next sections.

To quantify economic value correctly, six steps need to be performed.

Step 1: Identify the cost of the competitive product and process that consumer views as best alternative. The first crucial step is to put oneself in the eyes and in the shoes of customers and ask what they view as best alternative to the purchase of the product being analyzed. This need not be a physically similar product; in the end, most products are used to perform a certain function and to attain certain goals. Any product, process, and activity the customer could alternatively use can serve as reference product. As in most cases, several products and activities will be able to perform at least part of the functions examined, the economic value of a given product will have to be calculated against at least the principal two and three best alternatives.

It is important to note that the set of products used for comparison depends on the customer’s, not the company’s, assessment of available alternatives. For example, a com- pany in the agrochemical industry was inclined to think that customers used a competing product as their alternative upon which other products were judged and was surprised to learn that for a certain customer segment hand weeding was actually the preferred alternative.

Step 2: Segment the market. The first step of the process immediately leads to the second step of segmenting the market. Significant differences in economic value arise from the way in which customers use and value the product and from how they value their respective reference products. These differences result from differences in incremental value, which in turn, usually result from distinctive charac- teristics of the customer, the usage of the product, and environmental factors.

A company with a broad, fragmented product line, limited physical space for inventory, and rapid response times will assign a higher value to just-in-time delivery than a company with only one product line and ample space for inventories. This explains why those companies

most adept at implementing value-based pricing deci- sions—think of software and pharmaceutical compa- nies—know that there is no other way of gaining insight into sources of customer value than through observation and intense field research into the customer habits and requirements. Microsoft, for example, is known for hand- ing out beta-versions of its latest enterprise software products to particularly knowledgeable companies and customer segments. This form of free customer feedback is used to determine which features add most value and to gain a deep understanding on how different customer segments use and value the product.

Step 3: Identify all factors that differentiate the product from the competitive product and process. Products and services can create value for customers in a variety of different ways: reliability, performance, ease of use, longev- ity, life cycle costs, user and environmental safety, service (in terms of delivery reliability, delivery speed, and flexibility of deliveries), superior esthetics, prestige, and so on.

The notion of these differentiating factors is extremely closely related to the concept of competitive advantage. Duncan, Ginter, and Swayne (1998) define competitive advantage as ‘‘the result of an enduring value differential between the products and services of one organization and those of its competitors in the minds of customers.’’ Again, it is important to note that the customer, not the company, is the judge deciding on whether the differentiating factors are actually relevant to better satisfy his needs and ambi- tions. For companies, this means nothing less than to define quality the way the customer does.

Step 4: Determine the value to the customer of these differentiating factors. Once the tangible sources of differ- entiation have been identified, monetary values are assigned to these factors for each identified segment of the market. This process straightforward for high-priced industrial equipment, where expert sales personnel know how to quantify reduced failure rates, start-up costs, and life cycle costs in monetary terms to demonstrate the value of a certain product to actual and potential customers. An example will be given in the following section.

It is possible to obtain fairly accurate estimates of sources of customer value also for other goods and services. Conjoint analysis is a simple tool which aims to capture trade-offs in product features in a systematic way and to assign monetary values to specific attributes (Auty, 1995). Customers are presented with a set of two similar products differing in price and other qualitative features and are forced to indicate which set of attributes they prefer.

By presenting options such as (a) a lower price and no technical support and (b) a higher price coupled with support and guarantees, conjoint analysis is able to quantify the value of specific product and service attributes for a group of customers.

Anderson, Jain, and Chintagunta (1993) identify the following other customer value assessment tools, which can be used for quantification purposes: internal engineer, field value in use, indirect survey, focus groups, direct survey, benchmarks, compositional approach, and importance ratings. In their empirical analysis, they found that focus group value assessments and importance ratings are the most widely used methods, while conjoint analysis is reported to have the highest practical success rates.

Step 5: Sum the reference value and the differentiation value to determine the total economic value. The product’s economic value is simply the sum of the price of the reference product plus its differentiation value. As the price of the reference product and the value of differentiating attributes are likely to vary across customer categories, the result of this process is not likely to be one monetary value for any given product, but rather a ‘‘value pool,’’ reflecting the fact that different categories of customers will assign different values to the product examined.

Step 6: Use the value pool to estimate future sales at specific price points. Once the value pool and economic value profile of a market has been determined, sales estimates for different price points can be obtained. For each price point, sales can be expected to comprise a significant share of all market segments, which value the product higher than the specific price examined.

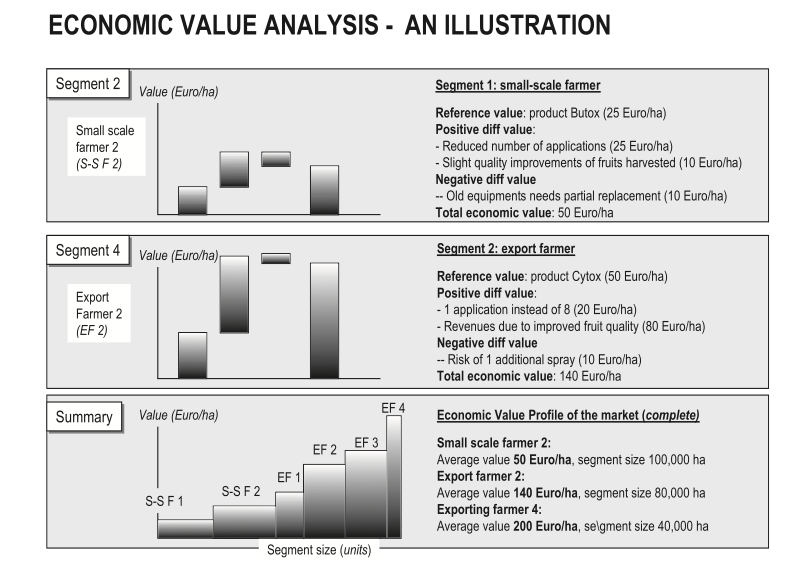

4.2.1.1. Economic value analysis illustrated. A leading agrochemical company faced the challenge of finding an appropriate price for the new, breakthrough insecticide Zenta used in the citrus market. By using the tool of economic value analysis, the market was divided in six segments: two seg- ments comprising small-scale farmers and four segments with mainly professional export farmers. For simplicity, the analysis will be presented for two market segments. For one segment of small-scale farmers, the reference product used is an off-patent product imported from China. Despite the broad spectrum of innovative features of Zenta—the extremely low dose rates and, thus, the low impact on the environment, among others—potential users in this segment value mainly the excellent efficacy of the product and the fact that the number of sprays is reduced from about 4 to just 1 per season. The other features were acknowledged as positive, but users were unwilling to pay for them.

A main concern of export farmers are residue levels of their products, which can severely hamper the ability to compete on international fruit markets. One key benefit of Zenta is the extremely low dose rate, in the order of magnitude of 1/1000 of a gram per kilogram of fruit, which makes the product ideally suited for low-environmental- impact treatments. In addition, professional export farmers value the fact that Zenta has a scientific track record of increasing the ‘‘pack-out ratio,’’ the percentage of oranges meeting the strict quality criteria of export markets. They also value the fact that, instead of having to use their tractor to spray in their orchards, they can apply the product by their drip-irrigation system, thus reducing mechanical dam- age on citrus trees. Zenta also reduces the total number of sprays from about eight per season—in the case of professional farmers—to just 1, which represents a significant cost and time factor.

On the negative side, the product carries the risk that on an occasion, and dependant upon insect infes- tation, one additional spray is required later in the season. This particular market segment values the economic benefits of Zenta at 140 Euro/ha, compared with 50 Euro/ha for the segment of small-scale farmers.

If these steps are applied to all six market segments, the economic value profile of the market can be determined. It indicates the total value created for each market segment and the segment size (in units). Fig. 4 illustrates these relationships.

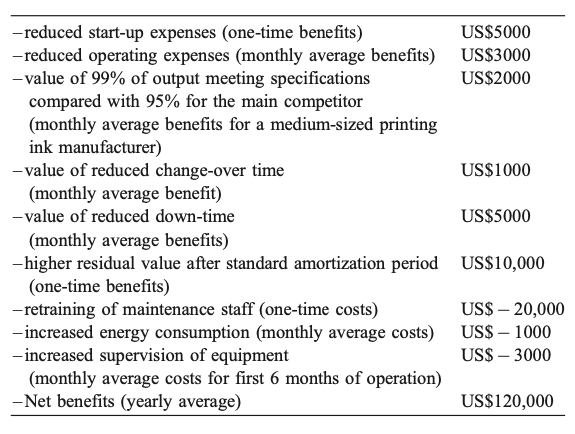

Another example of pricing decisions directly influenced by customer value analysis is the case of a Japanese industrial equipment manufacturer. In its home market, its standard model was priced at the equivalent of US$80,000 compared with US$50,000 for a similar model by its main competitor from the United States. Prices in the United States, the second largest market, were slightly different, although the same absolute price differential between the two models was maintained. In Japan, the company sold about 80% more units than its U.S. competitor, while in the United States, where the company had a weaker distribution system, both companies had roughly the same unit sales, although histor- ical growth rates of the Japanese company had by far exceeded the growth rates of its U.S. rival. What is the reason that the Japanese company was able to achieve both a high relative market share and a significant price premium?

The answer lies in a unique understanding of the sources of economic value to customers on the one hand, and in a superior ability to create and deliver this value to customers on the other hand. For each industry segment, the Japanese company had developed detailed financial models of different cost and benefit components of its own equipment versus its main competitor. For a customer in the printing ink industry, the positive and negative differentiation value was quantified in the following way:

Under this angle, the price premium of the Japanese company is modest. If an interest rate of 8% is applied to the net benefits gained over the average life cycle of this equipment of 4 years, the positive differentiation value amounts to well over US$300,000. Customers are expected to pay only a small fraction—less than 10% and US $30,000—of the product’s economic value.

Also in this case, the higher priced product ends up costing the customer less. This is an important lesson for industrial marketing managers: If economic value to customers is understood, quantified, and communicated, high prices and high relative market share can coexist.

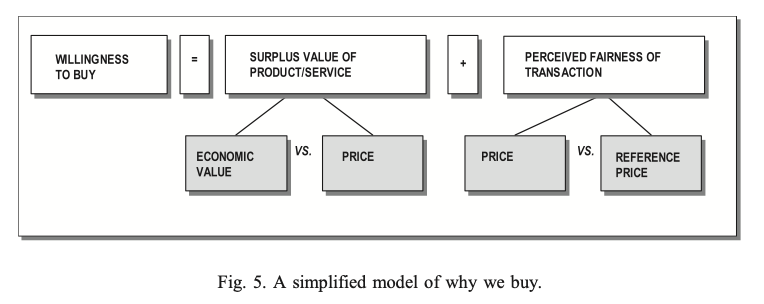

4.2.1.2. Why we buy. Rational purchase decisions do not rely exclusively on economic value versus price—also, the perceived fairness of the transaction plays a role in deciding whether a product with a certain perceived value is actually bought. A simplified model of buying behavior is presented in Fig. 5 (Thaler, 1985).

The surplus value of products and services is the difference between the economic value assigned to them and their price. The perceived fairness of the transaction is influenced by the price paid compared with internal refer- ence prices.

The internal reference price is simply the price and price level, which is expected and perceived to be ‘‘fair’’ for the product category in question (Smith & Nagle, 1995). Reference prices are held internally by customers, are formed over time, and reflect standard, that is, average prices for the category considered. The underlying premise is that consumers do not respond to prices absolutely, but rather relatively to the reference price (Thaler, 1985). When actual prices are evaluated against reference prices in purchasing transactions, consumers will frame the transac- tion as either ‘‘fair’’ or ‘‘unfair.’’ Take the example of the Japanese industrial equipment manufacturer just mentioned. Although the company could well have charged its custom- ers more than US$250,000 for its product while still offering them an attractive and financially interesting value propo- sition, it is likely that its customers would have been reluctant to pay a price premium of 600% over the best available alternative. Although fully convinced of the eco- nomic value of the product, it can be assumed that custom- ers would have perceived this transaction to be ‘‘unfair,’’ in the sense that the supplier would have been seen to attempt to capture the near totality of the benefits created via excessively high prices.

Pricing based on economic value analysis can lead to high relative price levels. Industrial marketers should re- member that the perceived fairness of the transaction is an important part of the purchasing mechanism. This leads to the natural caveat that the fairness of the transaction needs to be explained and demonstrated when pricing based on economic value leads to relatively high price levels.

4.2.1.3. Managing economic value. Economic value has a hard and a soft component: It is composed of a buyer’s best alternative, that is, a specifically identifiable product and process that the customer knows well and for which there is a clearly identifiable market price. It is also composed of the differentiation value, that is, a subjective source of value of the product’s attributes for the customer. In brief, economic value is not an inherent component of a product, but rather a trait, which can and should be managed. The succeeding sections discuss ways on how economic value can be managed.

Increase the value of the product’s perceived substitutes (substitution effect). Buyers are more price sensitive the higher the product’s price relative to the prices of the buyers’ perceived substitutes (Nagle & Holden, 1999).

The key word here is ‘‘perceived.’’ Perception varies widely among customers and across purchase situations. And of course, perceptions can be managed.

Effective marketing can position an expensive product as good value by selecting a high reference as comparison. Take the example of Loctite, an industrial adhesive, which is positioned as substitute for nuts and bolts.

Reference price expectations have an impact also at the point of sale. In stores where generic (no-name versions of off-patent products) and branded products are placed side by side for easy comparison, sales of low-priced products are usually much greater.

Emphasize the product’s unique value (unique value effect). Buyers are less sensitive to a product’s price the more they value any unique attributes that differentiate the product from competing products (Nagle & Holden, 1999).

For products and services with short development cycles (industrial insurances) a key lever of value creation lies in the development of new products meeting large, unmet needs. For products with longer development cycles (spe- cialty chemicals, cars) product development is, of course, important. However, in light of the fact that most salient product characteristics cannot be changed for years once the product is launched, a key leverage point for value creation in this case is the identification of customer segments who attribute the highest value to a given set of attributes.

The goal is to offer something ‘‘unique,’’ a differentiation that customers will pay for despite the existence of lower priced alternatives.

A frequent mistake is to analyze competitive products and to derive drivers of customer value from this analysis (Ohmae, 2000). Instead, it should be attempted to measure those factors that really matter for customers, irrespective of whether, currently, those needs are met by competitive products.

Lone Star Industries has launched an innovative concrete called Pyrament, a strong, extremely resistant, fast drying cement. Regular cement cures from 7 to 15 days, and a thick bed of cement is required for highways. Pyrament, by contrast, dries in a matter of hours and requires significantly less concrete per meter of construction. When the company analyzed pricing options for Pyrament, its unique benefits were considered and quantified. Highway operators would no longer be forced to shut down entire lanes of a highway for weeks for routine repairs, being able to reopen lanes just a few hours after repair works will have ended. Because shutdown time is expensive, the value proposition of Pyra- ment was built around this unique property of reducing downtime. Subsequently, prices were set between US$150 and 200 per ton compor traditional concrete.

Create switching costs between products (switching cost effect). Buyers are less sensitive to the price of a product the greater the added cost (both monetary and nonmonetary) of switching suppliers. The greater the product-specific investments that a buyer must make to switch suppliers, the less price sensitive a buyer is when choosing between alternatives (Nagle & Holden, 1999).

Where the service component is important, personal relationships with qualified sales personnel can represent a significant switching cost. Where a long-term relation- ship between customers and suppliers is feasible, suppliers can invest in infrastructure to fortify the bonds with customers. With the implementation of automated parts ordering based on inventory levels, suppliers in the auto- motive industry have created strong links with present customers thus increasing switching costs and entry bar- riers substantially.

B2B on-line retailers have created significant switching costs between their brands and their competitors through in-depth customer knowledge. Information on customer preferences, tastes, and purchase histories are stored elec- tronically and clearly reduce the incentive to switch. Render comparisons between products difficult and impossible (difficult comparison effect). Buyers are less sensitive to the price of a known reputable supplier when they have difficulties comparing alternatives (Nagle & Holden, 1999).

All efforts of product differentiation can be interpreted as measures to render comparisons between brands as difficult. The capacity to create a differentiated product is confined by the limits of imagination. Even producers of commodities differentiate themselves by the amount, the extent, and the speed of service they provide to customers. Services are, of course, a key component of the strategies of all manufacturing companies. Look at GE, a company

that has decided to transfer its unique knowledge of 6 Sigma and M&A expertise to the businesses of its customers, where GE personnel implement the traditional GE practices at the customers’ premises.

Increase prices (price–quality effect). Buyers are less sensitive to a product’s price to the extent that a higher price signals better quality (Brucks, Zeithaml, & Naylor, 2000).

Price carries two connotations (Leavitt, 1954). It is not only the monetary sacrifice that is necessary to obtain a product but, in its positive connotation, it can signal the quality of the product and it can confer to its owner an aura of prestige (Dodds, Monroe, & Grewal, 1991).

When product quality is difficult to assess and when provided with a brand name, potential buyers will rely on price to infer quality. In this case, a higher price signals higher quality.

Although a general relationship between price and quality levels has not been found in empirical studies (Zeithaml, 1988), it has been confirmed that consumers will rely on price when they have little experience with the product and when they cannot readily evaluate intrinsic product attributes.

For products perceived to be superior along a critical performance dimension, this effect strongly suggests the opportunity of building a brand name. It is impossible and damaging to a company’s credibility to build a brand with an inferior product. If, however, the product is superior in some important way, a brand name creates value for customers. Similar to insurance, it offers a guarantee for consistent reliability and performance. Higher prices for brands versus no-name competitors add value for both the customer and the company.

This effect is even more important when ownership and use of the product can be associated with prestige. Consider the case of an industrial chemicals company, which faced competition from a no-name brand from China in one of its core markets. The two products were similar, and the price differential was 4 to 1. In what seemed like a lost war, the company positioned its product as ‘‘the product for the country’s most progressive users.’’ Development activities were directed to move the product away from its compet- itor through innovative formulations, and the product was able to increase its market share despite subsequent price cuts by its Chinese competitor.

Relate the product to an important end-benefit (end- benefit effect). Customers are less price sensitive whenever the purchase price accounts for a smaller share of the total cost of the end-benefit (Nagle & Holden, 1999). The higher the end-benefit to which the product is related, the lower the price sensitivity of customer is expected to be. This effect shows the opportunity of very high prices for products related to an important end-benefit and sold to complement much larger purchases.

Antitrust lawyers, for example, successfully sell exorbitant hourly rates for legal advice in mergers and acquisitions as an insurance against the devastating effects and heavy fines of antitrust lawsuits by the European Commission and the Federal Trade Commission.

Marketers can use this strategy also when the risk of failure is very high and when they can persuade customers to perceive the risk as high. Car manufacturers have largely succeeded in this approach in the market of original versus no-name spare parts.

Be fair (or, at least, create the impression of being so). As outlined above, the perceived fairness of the transaction plays a key role in determining the willingness to buy.

Prospect theory (Kahnemann & Tversky, 1979) has argued that individuals evaluate expected outcomes from decisions in terms of gains and loses from a reference point, where losses have larger negative utility than gains of the same amount, thus, proposing a utility function that is steeper for losses than for gains. Decision makers judge a loss as more painful as they judge a gain of equal amount as pleasurable.

Marketers have used these findings to suggest that prod- ucts should be positioned in such a way to offer potential customers a gain rather than merely preventing a loss. Insurance companies, security agencies, and IT companies, for example, seem to have followed this advise. Remote data backup companies offer ‘‘peace of mind and tranquility’’ rather than preventing theft and loss of valuable data. Sim- ilarly, fleet management companies advertise their services nearly exclusively as a means to gain control and visibility over expenses rather than as a means to prevent problems, something customers are more likely to resent to having to pay for.

Prospect theory is also very useful when marketers are confronted with the problem of having to justify steep price increases. They can obscure the reference price by selling in unusual packages, formats, and quantities. They can also implement the price increase in two steps: In a first step, a discount is offered on an increased price for a certain period of time. Subsequently, the discount is eliminated. In this way, consumers will experience a gain from benefiting from the initial price reduction, rather than being confronted at once with a steep increase.

4.2.2. Cost volume profit (CVP) analysis

Having analyzed the customer perspective, the attention is now on the company itself and its cost structure.

It is surprising how few executives are able to answer the following question: ‘‘If prices are raised by 10%, how much turnover can the company afford to lose, if overall profits are at least to be maintained?’’

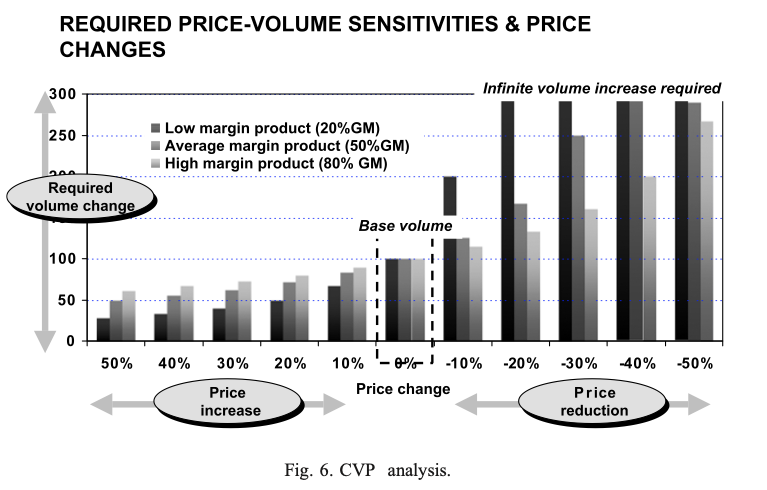

The answer to this question depends exclusively on a product’s profitability, that is, on its contribution and gross margin (net sales revenues less variable expenses). CVP is analysis the tool designed to perform this analysis (Guidry, Horrigan, & Craycraft, 1998). A look at Fig. 6 reveals the necessary sales increase/maximum sales reduction for contemplated price reductions/price increases for different levels of product profitability (20 – 50 – 80% gross margin). For products with 20% contribution margins, for example, a price reduction of 10%, which manufacturing companies generally consider to be low-margin products, would have to translate into a 100% increase in sales to be profitable.

On the other hand, for products with contribution mar- gins of 70%, a price increase of 10% is profitable if sales decline by 13% and less.

The formula for CVP calculations is the following (Smith & Nagle, 1994):

Break even sales change (%)

CVP analysis is a simple, yet powerful tool to assess whether contemplated price changes have any chance of being profitable for the company. Low-margin products usually require fairly large volume increases for price reductions to be profitable; it should thus be considered to either increase/maintain the price and to exit. For high- margin products, on the other hand, price increases can be quite profitable, if volumes are expected to decline less than the amount indicated in Fig. 6.

CVP analysis can even be refined to incorporate fixed costs, for example, if a promotional campaign is associated with the planned price reductions and price increases.

The analysis can be split up in two steps.

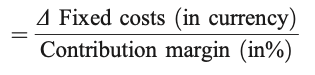

1. The necessary volume increase for fixed costs investments is treated as separate issue via the following formula:

Break even ???? sales change (in currency)

Let us assume that investments for a promotional campaign and for hiring and training additional sales reps amount to 50,000 Euro, and that the product in question has a 50% contribution margin. In order for this invest- ment to be profitable, sales would have to increase by 100,000 Euro.

2. In a next step, planned price changes can be analyzed together with planned fixed costs investments:

Break even ???? sales change (%)

Again, CM stands for contribution margin and ‘‘new’’ unit contribution margin refers to the contrition margin after the planned price change. An example will clarify the possibly confusing equation.

If a price reduction of 10% is planned and if 50,000 Euro are needed to communicate the special offer, how much additional sales are necessary in order for the price reduction to be profitable?

If the initial unit price is 10, and if initial unit sales amount to 100,000, the equation will give the following results:

Break even ???? sales change (%) = +25 % + 13)% = – 8%

If sales decrease by 8% and less, a 10% price increase is profitable, even with the substantial investments in promotional activity. The exercise here confirms a common-sense assumption; however, also seasoned executives often fail to understand the amount of turnover increase required to aggressively promote and sell lower margin products.

4.2.3. Competitive analysis

The third cornerstone of profitable pricing decisions is competitive analysis. The following elements should be covered in this process.

4.2.3.1. Threat of new entrants. Even before analyzing current competitors, managers need to understand and evaluate the threat of new competitive entry. Pricing decisions, which are based purely on the economic value delivered to customers, may lead to price levels high enough to attract new competitive entry. Specifically, the threat of new entrants will depend on factors such as access to distribution channels, access to raw materials, technical barriers to entry, customer’s propensity to switch, and quality differentials between incumbents and new entrants. All these factors have to be analyzed in the context of competitive analysis.

4.2.3.2. Price trends in existing markets. Prices and price trends in major market segments should be monitored very carefully to know where the market is and where it might be going in the future. Especially in industrial markets, it is not uncommon for customers to deliberately lie to sales person- nel about prices offered by competitors. In doing so, they hope to obtain larger discounts and more favorable selling terms. Without a reliable database of competitive informa- tion, the sales personnel is frequently tempted to lower prices to win the order, thus, potentially destroying price levels in the market and starting a price war which all competitors would have liked to avoid. The only way out of this dilemma is to instruct sales personnel to collect infor- mation about price levels, price trends, and competitive sales personnel on a regular basis. This will allow to spot trends quickly and to steer sales personnel and their pricing policies much more effectively.

4.2.3.3. Competitive strategies. Principal market segments should be analyzed with strategies of competitors, estimat- ed profitability across principal product lines and market segments, future expansion plans, strengths and weak- nesses in different segments, and anticipated future com- petitive behavior. The following are questions to be answered: Which of the current market segments and/or customers are threatened most by the strategies of com- petitors? What is the answer? How can stability and profitability of industry be preserved? How can price wars be avoided?

4.2.3.4. Information about distribution channels. Relevant information here includes: market share with key distrib- utors, amount of products stored in distribution channels, pricing and payment policies of distributors, incentive schemes of principal competitors, sales forecast from selected distributors, competitive activities with distributors (promotions, new product launch initiatives), etc.

4.2.3.5. Reference values for customer groups. Economic value analysis relies heavily on the notion of reference value, that is, the customer’s best alternative to the product being acquired. Different clusters of customers will invari- ably take a different product as reference value for the purchase in question. In addition, customer preferences change over time. It is therefore critical to obtain reliable information about different reference values and about the competitive products behind them to be able to develop effective pricing strategies.

4.2.3.6. Likely reactions to price changes. If the economic value and CVP analyses suggest price increases on some products it is essential to anticipate likely reactions of competitors to these price changes. Is there a way to ‘‘test the waters’’ before implementing any significant price increases?

5. Determine a range of profitable prices

Economic value analysis, CVP calculations, and com- petitive intelligence provide the cornerstones of effective pricing strategies. With this information in mind, the justi- fication, the magnitude, and the impact of price increases can be estimated. If, for example, economic value analysis suggests to reposition the product and to increase prices by 30%, CVP calculations can be used to determine the maximum amount of affordable volume loss. For a product with a 70% margin, this price increase is profitable if volumes decline by less than 30%.

Now, feedback from sales managers, marketing staff, distributors, and a sample of customers is gathered to assess whether the actual volume loss is likely to be larger and smaller than this number. If exploratory research suggests that the actual customer price elasticity is lower and that the predicted volume loss is 15 – 20%, managers have a strong case for implementing the contemplated price increase.

6. Implement prices changes

Once the magnitude of a price increase (or price reduc- tion) has been determined, it has to be implemented.

The sales force has the key task of justifying, communi- cating, and implementing these price changes—in addition to the responsibility of proactively discussing with headquarters the issue of any price alterations whenever necessary.

It is an interesting and well-known truth—at least among executives with a sales background—that there is no way of controlling sales personnel in the field; whatever instructions on recommended product use, positioning and price they might have received, managers in the head office cannot be 100% sure that these instructions are actually followed. The reason is that there are simply too many temptations for attempting to win a sales order in an unorthodox way. In informal discussions with customers, sales managers might be tempted to suggest, for example, nontraditional ways of using the product (think of the widespread off-label usage of drugs in the pharmaceutical industry). In the worst case, they might suggest to the customers that the recently implemented price increase is nothing else than headquar- ters’ version of attempting to increase profits at the expense of customers, and that, if several large accounts refuse to sign any orders, the price change will be reversed in the next 3 months.

Sales personnel have the potential to fortify and to destroy any planned price changes. It is therefore vital to manage the sales force well. Several issues should be considered.

6.1. Involve sales executives in any pricing decisions

Nothing can be more frustrating for sales personnel than having to confront a long-standing customer—and, therefore, potentially also a friend—with the fait accompli of a significant and sudden price increase. Before imple- menting any price changes, sales personnel should be asked to contribute to the debate. Rather than being given the impression of having to execute a decision from headquarter, sales managers should truly feel that they are acting on nothing else than their fullest conviction. They need to have a full say in pricing and other marketing issues. Otherwise the Roman proverb ‘‘Whoever is not working with you, is working against you’’ might just come true.

6.2. Implement a fixed-price policy

Stephenson, Cron, and Frazier (1979) have investigated whether salespeople with no authority to deviate from list prices, those with limited authority to deviate from list prices, and those with full discretion with regard to pricing generate the highest gross margins for their companies. Probably unsurprisingly, they find that firms that give sales personnel the least pricing authority generate the highest levels of gross margin.

Fixed-price policy encourages sales personnel to sell on value and not on price. A fixed-price policy does not mean that all customers actually pay uniform prices: Segmented pricing—by type of customer and distribution channel—can complement a policy of fixed prices. In this way, sales managers have the flexibility of adapting prices to different types of customers and distribution channels, but the criteria of this segmentation are out of their hands. Marketing and sales managers in headquarters make sure that this segmen- tation is consistent across sales territories and reflects the strategy of the company.

6.3. Reward sales personnel for profits and not sales

Sales personnel have to be rewarded for selling value. Consequently, rewards should be linked to margin gener- ated and not to turnover. Despite this fairly obvious conclusion, it is frustrating to see how biased current compensation schemes are towards selling volume. In an in-depth survey of large manufacturers, McKinsey found that 80% of companies base their compensation and incentive scheme for sales managers exclusively on rev- enue (Alldredge, Griffin, & Kotcher, 1999). Only a minority of companies link compensation to any form of profitability. If executives feel that product margins should not be fully shared with sales personnel, the compensation scheme can be based on a simple point scheme. Points should then reflect product and account profitability.

6.4. Involve sales personnel in the strategy process

Besides soliciting proactive input from sales managers on pricing, executives should attempt to involve the sales force in other aspects of strategy. Sales managers should be involved in the late stage of the new product devel- opment process for feedback on product attributes and features; they can also help headquarter to identify lead customers, that is, those customers particularly able to sense market trends and help the company adapt its strategy to changing environmental conditions.

6.5. Be creative with marketing strategies

Except for the packaged goods industry and apparel, where some of the most creative and expensive advertising campaigns come from, creative marketing strategies are still easy and cheap to implement. Chemicals, banking, consult- ing, etc. still have much room for creative marketing practices. Price and product bundling, for example, should be used wherever it adds value for the customer and offers the potential to stimulate sales.

6.6. Make the company easily accessible for customers

Not only Internet-based stock brokerages, but also car manufacturers, pharmaceutical companies, insurance com- panies, and the like should consider offering 24/7 hours call center to actual and potential customers.

Many companies still have a lot to learn in the way customer complaints are handled. It is frustrating to see that in many companies, even ridiculously small amounts of products offered in return to complaints have to be approved by headquarters. In addition, here, sales man- agers need to be given far more discretion, informing their supervisors only periodically, rather than having to explain customers the complicated routes of refunds policies.

6.7. Commercial and technical personnel should converge

In many companies, commercial personnel is expected to facilitate transactions, while technical personnel is expected to intervene in cases of new product launches, complaints, and difficult questions. In the end, sales people sell and technical people, well, have a technical and R&D background.

This distinction can be outdated and wasteful. It leads to technical personnel being comfortable in research laborato- ries, but only remotely familiar with real customer issues and to sales personnel unwilling to keep up to date with the leading edge of science in their field. By broadening the function of sales personnel to include full accountability on all technical issues, companies can both streamline their customer interface and reduce costs.

7. Conclusions

Everything is worth what its purchaser will pay for it.

Publius Syrus, First Century, B.C.

This paper presented a coherent framework, which will lead to the implementation of a value-based pricing strat- egy. After taking a company’s objectives into consideration, it is suggested to use the tools of economic value analysis, cost-volume profit analysis, and competitive analysis to reflect the customer, company, and competitor perspective relevant for all strategic decisions. As a result, ranges of profitable prices are determined. In the last step, the price change is implemented. Pricing is a process with a feed- back loop. Assumptions need to be revisited, and environ- mental dynamics need to be taken into consideration, which makes it necessary to reiterate the steps outlined.

The main focus of the paper is a process which has been called economic (or customer) value analysis. It has been argued that a solid understanding and quantification of customer value is a key to profitable pricing. This understanding can suggest where to increase prices with- out risking to lose sales. Customer value analysis is a tool, which can be used to justify price increases to customers; it can also help in the new product develop- ment process.

With this, it is evident that a relentless focus on competitiveness can have major drawbacks: Instead of attempting to create and to communicate value to custom- ers, companies risk paying an unjustified attention to current product features of competitors, regardless of whether they meet customer requirements and truly create superior customer value.

Empirical research strongly support this claim: In a field study involving 20 U.S. firms over an extended period of time, Armstrong and Collopy (1996) find that companies with a pure competitor-oriented strategy are less profitable and less likely to survive than companies with a strong customer orientation. They conclude that the use of compet- itor-oriented goals can be detrimental to profitability.

Differentiation from competitors does not per se add value. It might lead to a sustained investment in product features, which do not add any value for customers. Product differentiation strategies have to be preceded by an under- standing of the real sources of value for customers, which then will lead to appropriate positioning and pricing. Eco- nomic value analysis is a valuable tool even when products are relatively undifferentiated; in this case, insights in the way in which the product adds value can lead to ways to develop the product further and to position it in ways which add value to customers.

Acknowledgements

The author wishes to thank the editor and the anonymous reviewers for their helpful comments on earlier versions of this paper.

References

Alldredge, K. G., Griffin, T. R., & Kotcher, L. K. (1999). May the sales force be with you. McKinseyQuarterly, 3, 110 – 121.

Anderson, J., Jain, D., & Chintagunta, P. (1993). Customer value assess- ment in business markets—A state-of-practice study. Journal of Busi-ness-to-BusinessMarketing, 1(1), 3 – 20.

Armstrong, J. S., & Collopy, F. (1996). Competitor orientation—Effects of objectives and information on managerial decisions and profitability. JournalofMarketingResearch, 33(2), 188 – 199.

Auty, S. (1995). Using conjoint analysis in industrial marketing—The role of judgement. IndustrialMarketingManagement, 24, 191 – 206.

Avila, R., Dodds, W., Chapman, J., Mann, K., & Wahlers, R. (1993). Importance of price in industrial buying. Reviewof Business, 15(2), 34 – 48.

Brucks, M., Zeithaml, V., & Naylor, G. (2000). Price and brand name as indicators of quality dimensions for consumer durables. Journal of theAcademyofMarketingScience, 28(3), 359 – 374.

Clancy, K., & Shulman, R. (1993). Marketing with blinders on. Across theBoard, 3, 33 – 38.

Dickson, P. R., & Sawyer, A. G. (1990, July). The price knowledge and search of supermarket shoppers. JournalofMarketing, 54, 42 – 53.

Dodds, W., Monroe, K., & Grewal, D. (1991). Effects of price, brand, and store information on buyers product evaluations. Journal of MarketingResearch, 28, 307 – 319.

Duncan, W. J., Ginter, P. M., & Swayne, L. E. (1998). Competitive ad- vantage and internal competitive assessment. AcademyofManagementExecutive, 12, 6 – 16.

Flint, D., & Woodruff, R. (2001). The initiators of changes in customers’ desired value—Results from a theory building study. IndustrialMarket-ingManagement, 30, 321 – 337.

Forbis, J. L., & Mehta, N. N. (1983). Value-based strategies for industrial products. BusinessHorizons, 24(3), 32 – 42.

Forbis, J. L., & Mehta, N. T. (2000). Economic value to the customer.

McKinseyQuarterly, 3, 49 – 52.

Golub, H., & Henry, J. (2000). Market strategy and the price-value model.

McKinseyQuarterly, 3, 47 – 49.

Guidry, F., Horrigan, J., & Craycraft, C. (1998). CVP analysis—A new look. JournalofManagerialIssues, 10(1), 74 – 85.

Hoch, S., Dreze, X., & Purk, M. (1994, October). EDLP, Hi – Lo, and margin arithmetic. JournalofMarketing, 58, 16 – 27.

Kahnemann, D., & Tversky, A. (1979, March). Prospect theory—An analysis of decision under risk. Econometrica, 47, 263 – 291.

Lamb, C., Hair, J., & McDaniel, C. (2000). Marketing (5th ed.) (Cincinnati, OH), South-Western College Publication.

Leavitt, H. (1954). A note about some empirical findings on price. JournalofBusiness, 27, 205 – 210.

Malhorta, N. (1996). The impact of the academy of marketing science on marketing scholarship—An analysis of the research published in JAMS. JournaloftheAcademyofMarketingScience, 24(4), 291 – 298.

Nagle, T. T., & Holden, R. K. (1999). Strategy and tactics of pricing. (2nd ed.). Englewood Cliffs, NJ: Prentice-Hall.

National Institute for Health Care Management (NIHCM) Foundation (2001). Prescription drug expenditures in 2000—The upward trendcontinues, NIHCM Report, Washington, DC.

Ohmae, K. (1982). The mind of the strategist—The art of Japanese busi-ness. New York: McGraw-Hill.

Ohmae, K. (2000). Getting back to strategy. McKinsey Quarterly, 3, 57 – 60. Pharmaceutical Research and Manufacturers of America (PhRMA) (2001).

Annualsurvey2001, New York.

Priem, R. L. (2000). The business level RBV: Great wall and Berlin wall?

AcademyofManagementReview, 26, 499 – 501.

Reichheld, F. (1996). The loyalty effect: The hidden force behind growth,profits, and lasting value. Cambridge, MA: Harvard Business School Press.

Shipley, D., & Jobber, D. (2001). Integrative pricing via the pricing wheel.

IndustrialMarketingManagement, 30, 301 – 314.

Simon, H. (1999). Pricing as a Strategic Weapon, Presentation at PRICE- PRO 1999, 25 – 26 January.

Simpson, P., Siguaw, J., & Baker, T. (2001). A model of value creation— Supplier behaviors and their impact on reseller-perceived value. Indus-trialMarketingManagement, 30, 119 – 134.

Smith, G., & Nagle, T. (1994). Financial analysis for profit-driven pricing.

SloanManagementReview, 35(1), 71 – 84.

Smith, G., & Nagle, T. (1995). Frames of reference and buyers’ per- ceptions of price and value. CaliforniaManagementReview, 38(1), 98 – 116.

Stephenson, R., Cron, W., & Frazier, G. (1979). Delegating pricing author- ity to the salesforce—The effects on sales and profit performance. JournalofMarketing, 43(1), 21 – 28.

Thaler, R. (1985). Mental accounting and consumer choice. MarketingScience, 4(3), 199 – 214.

Ulaga, W., & Chacour, S. (2001). Measuring customer-perceived value in business markets—A prerequisite for marketing strategy and implemen- tation. IndustrialMarketingManagement, 30, 525 – 540.

Walter, A., Ritter, T., & Gemuenden, H. G. (2001). Value creation in buyer – seller relationships—Theoretical considerations and empirical results from a supplier’s perspective. Industrial Marketing Manage-ment, 30, 365 – 377.

Zeithaml, V. (1988). Consumer perceptions of price, quality, and value: A means– end model and synthesis of evidence. JournalofMarketing, 52, 2 – 22.