Abstract

This study explores the origins and benefits of value quantification capabilities in industrial markets. After polling 131 US industrial sales and account managers, this study finds that value quantification capabilities improve firm—but not individual sales manager—performance. Second, in stable markets, the effect of value quantification capabilities on firm performance is stronger than in dynamic markets. Third, the study finds that the following psychological traits are positively related to the individual value quantification capability: risk taking and creativ- ity, sales manager questioning style, customer-oriented selling, and cross-functional collaboration. This study suggests that value quantification capabilities benefit firm performance especially in stable markets, it explores attitudinal and behavioural traits underlying value quantification capabilities, and it highlights the need for fur- ther studies exploring the circumstances under which value quantification capabilities improve individual sales manager performance.

© 2017 Elsevier Inc. All rights reserved.

1. Introduction

What sets pricing in business markets apart? After all, the activities required for effective pricing in consumer markets—an analysis of cus- tomer needs, customer willingness to pay, competitive advantages, competitor price levels, and cost structures—are equally relevant for pricing in business markets. What is it that fundamentally distinguishes pricing in B2B from pricing in B2C?

The fundamental difference is this: in business markets, pricing is all about quantifying value, documenting that the price is less than the quantified sum of customer benefits. Anderson, Narus, and Van Rossum (2006, p. 96) observe: “To make customer value propositions persuasive, [B2B] suppliers must be able to demonstrate and document them.” Value quantification is clearly not necessary in consumer mar- kets: Coca Cola does not have to quantify to customers that its price pre- mium over its main competitor—typically around 10%—is less than the incremental customer value provided. Individual consumers implicitly make this value quantification and then decide accordingly (i.e., pur- chase/no purchase).

In B2B, by contrast, purchasing managers quantify the value of alter- native offers in their supplier selection decisions (Plank & Ferrin, 2002). In addition, these purchasing managers demand that B2B sellers them- selves quantify value: A survey of 100 IT buyers at Fortune 1000 firms reveals that 81% of buyers expect vendors to quantify the financial value proposition of their solutions (Ernst & Young, 2002); a subsequent survey asks 600 IT buyers about major shortcomings in their suppliers’ sales and marketing organizations (McMurchy, 2008): IT buyers consid- er an inability to quantify the value proposition and an inability to clarify its business impact as important supplier weaknesses. These surveys indicate that purchasing managers consider the ability to quantify the financial impact of the value proposition as very important in the ven- dor selection process. How well do sales managers quantify value? Both practitioner (Ernst & Young, 2002) and academic research (Anderson, Kumar, & Narus, 2007; Hinterhuber, 2008) suggest that most companies struggle to convert their value propositions into quan- tified customer benefits. There is thus a gap between the capabilities that industrial buyers demand and the capabilities that industrial sellers have regarding value quantification.

This gap raises a question: Does value quantification improve perfor-mance in industrial markets? Academic research suggests that it does; however, sparse evidence from practitioners appears, surprisingly, mixed. Qualitative research indicates that the performance of sellers in B2B—measured via realized price levels and win rates—improves as a result of value quantification (Anderson, Narus, & Narayandas, 2008; Töytäri, Brashear, Parvinen, Ollila, & Rosendahl, 2011). Practitioners are split on the question of whether value quantification is beneficial in B2B. On one side, companies such as SKF, SAP, HP, Grainger, Metso, Applied Industrial, Maersk and others recognize the benefits of value quantification. Tom Johnstone (2007), CEO of SKF, states: “One of the most important tasks we have today throughout the SKF Group is to cre- ate, deliver, and document the value that our products and solutions bring to our customers.” Similarly, Matti Kähkönen (2012, p. 21), CEO of Metso, says: “Understanding of customers’ businesses and KPIs [key performance indicators] create[s] a solid basis for quantifying the busi- ness impact for the customer.”

Other industrial companies, such as Black & Decker, seem to take a different view: having lost its position as market share leader to Makita, the company regained the number one position in industrial power tools in the mid-1990s in one of marketing history’s most spectacular turnarounds. A key element of Black & Decker’s strategy, the launch of DeWalt in the professional power tool market, was an exclusive focus on product attributes, specifications, and features in marketing commu- nication, thus leaving it to B2B customers themselves to understand and quantify value (Dolan, 1998). Communicating product benefits and value risked, according to Joe Galli, VP of marketing and sales, “consumerizing” an essentially industrial product (Dolan, 1996).

Contrasting views on the benefits of value quantification are evident also from the interviews underpinning this study. One interviewee (Hinterhuber & Heutger, 2017, p. 154) suggests that value quantifica- tion is always beneficial (see Section 3 for details):

And even if you’re not obliged to quantify the value to get the busi- ness, I would still advocate doing it. You can always go to the cus- tomer at a later date and say, “Hey! Look, this is what we did for you.” This certainly helps to keep customers loyal and increase re- newal rates . … I think it [i.e., value quantification] does always work. [Heutger, SVP Strategy and Marketing, DHL]

Another interviewee suggests that value quantification is not bene- ficial in highly commoditized markets (see Section 3 for the detailed quote). According to that interviewee, the benefits of value quantifica- tion are contingent on market characteristics.

Once again: Does value quantification always influence firm perfor- mance? And if so, under which circumstances are value quantification capabilities less beneficial? The existing literature does not appear to answers these fundamental questions. If value quantification indeed benefits firm performance, it should be clear what makes some sales managers more effective and others less so in value quantification. It is not. The purpose of the present study is to explore whether value quantification improves sales performance in B2B.

To answer these questions, this study surveys 131 US B2B sales and account managers to explore antecedents and consequences of value quantification. This study finds that value quantification capabilities are positively related to firm—but not to individual sales manager—performance. The data also suggest that this positive rela- tionship is weaker in highly dynamic markets. Finally, this study iden- tifies the psychological characteristics and behaviors at the level of the individual sales and account manager that are positively related to the value quantification capability. These characteristics are risk taking and creativity, sales manager questioning style, customer-oriented sales, and cross-functional collaboration. This study contributes to the understanding of the micro-foundations of value quantification capabil- ities at the level of individual sales managers and highlights the benefits of quantifying value in industrial markets. The study finally points to- wards the need to better understand the relationship between individ- ual value quantification capabilities and individual performance.

2. Theoretical foundations

Three main research streams constitute the theoretical foundations of this paper: research on customer value, on selling, and on value- based pricing. Keränen and Jalkala (2013) and Terho, Haas, Eggert, and Ulaga (2012) provide thorough summaries of the literature on cus- tomer value: in line with earlier research equating value with customer benefits received (Zeithaml, 1988), scholars nowadays tend to concep- tualize value in B2B as the incremental impact of a supplier’s offer on the customer’s own bottom line (Nagle & Holden, 2002). Value in business markets “is the worth in monetary terms of the economic, technical, ser- vice, and social benefits a customer firm receives in exchange for the price it pays for a market offering” (Anderson et al., 2008, p. 6). Custom- er value is the maximum amount that a customer is willing to pay to obtain the supplier’s products and services. In B2B, customer value comes in two forms: quantitative customer benefits (i.e., cost reduc- tions, margin improvements, risk reductions, capital savings) and qual- itative customer benefits (e.g., intangible advantages). Value in B2B is subjective, customer-specific, relative to the customer’s best alternative, discovered collaboratively with customers, and expressed in monetary terms.

Value and price are two separate constructs: changing one does not change the other (Hinterhuber, 2004; Wouters, 2010). The critical capa- bility in industrial markets is value quantification or value visualization (Kindström, Kowalkowski, & Nordin, 2012): “Understanding customer value in business markets involves monetary quantification of the ben- efits of a firm’s offering, yet, from the perspective of the customer firm” (Wouters, 2010, p. 1101). “A key to becoming part of customers’ strate- gic agenda is the ability to quantify the business impact” (Storbacka, 2011, p. 706). Value quantification is necessary because customers, by themselves, generally fail to recognize value even when they see it: “One of the great misconceptions of quantitative pricing research is that customers who have been using a product know what it is worth to them without being told” (Nagle & Cressman, 2002, p. 33).

Value quantification is thus an important communication tool. Current research suggests that high-performing companies quantify and document value (Anderson et al., 2007; Anderson et al., 2008; Töytäri & Rajala, 2015), but so far this claim has not been substantiated by quan- titative evidence. It is—in theory at least—possible that value quantifica- tion is an intellectually appealing idea where isolated cases of success studies mask the fact that for most companies the pursuit of this strate- gy substantially reduces performance, as is true for the popular concept of solution selling (Krishnamurthy, Johansson, & Schlissberg, 2003; Roegner & Gobbi, 2001). It is furthermore possible that the benefits of value quantification are contingent on firm-specific or environmental factors.

Research on selling has witnessed a surge of interest only recently.

Traditionally, top marketing journals published a small and declining number of papers on sales management (Plouffe, Williams, & Wachner, 2008; Richards, Moncrief, & Marshall, 2010). This situation has changed: current research recognizes the importance of selling and finds that how selling is performed has a substantial impact on company performance (Haas, Snehota, & Corsaro, 2012). Among differ- ent approaches to selling that the literature discusses (Terho et al., 2012), value-based selling is most pertinent to the current study. Value-based selling comprises several overlapping steps: customer identification, customer needs analysis, value proposition development, value quantification, value-based pricing, post-delivery value verifica- tion and documentation, and development of case repositories (Terho et al., 2012; Töytäri & Rajala, 2015; Töytäri et al., 2011). Value quantifi- cation is a cornerstone and, at the same time, the “biggest challenge” of value-based selling (Töytäri & Rajala, 2015, p. 105). The literature exam- ines the capabilities (Töytäri & Rajala, 2015) and performance implica- tions of value-based selling (Terho, Eggert, Haas, & Ulaga, 2015). The factors that enable sales managers to quantify value, however, are yet to be fully explored.

The value quantification capability refers to the ability to translate a firm’s competitive advantages into quantified, monetary customer benefits. The value quantification capability requires that the sales man- ager translates both quantitative customer benefits—revenue/gross margin increases, cost reductions, risk reductions, and capital expense savings—and qualitative customer benefits—such as ease of doing business, customer relationships, industry experience, brand value, emotional benefits or other process benefits—into one monetary value equating total customer benefits received. Value quantification de- mands more from sales managers than merely quantifying the total cost of ownership (Piscopo, Johnston, & Bellenger, 2008).

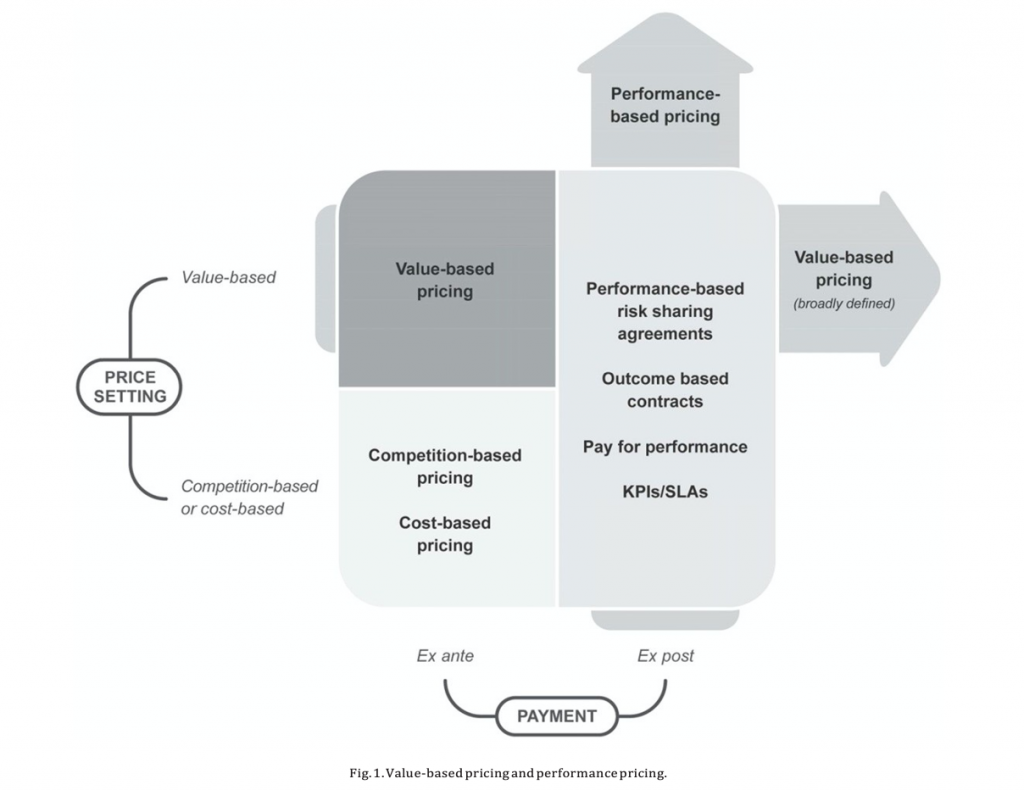

An important clarification concerns the relationship between value- based pricing and performance pricing. Value-based pricing refers to an ex-ante payment scheme where prices reflect customer willingness to pay or expected customer profitability improvements (Nagle & Holden, 2002). Performance-based pricing approaches are arrangements where prices are adjusted ex post, as a function of predefined indicators of product or customer performance. Value-based and performance- based pricing are two separate constructs. The distinctive element is risk transfer. In value-based pricing, customers assume the full risk or benefit of performance variations. In performance-based pricing, risk is shared between the customer and the supplier. Fig. 1 illustrates the relationship between pricing approaches (cost-, competition-, and value-based) and payment (ex ante, ex post).

Industrial companies, such as Arcelor Mittal, DSM, GKN, Monsanto, Roche, SKF, Stanley Black & Decker, Würth, and many others set prices based on the incremental, expected performance advantages of their offerings to specific customers. These companies all set prices ex ante. In the steel industry, for example, prices reflect use value, which is determined by a range of factors including chemistry, mineralogy, and application (Ridsdale, 2011). Value-based pricing at DSM involves understanding customer-specific switching costs and perceived differ- entiation (Adade & Simonetti, 2013). There generally is no ex-post ad- justment based on actual versus expected performance. In all these instances, value quantification is extremely important: it documents to customers that the price difference versus the customer’s best avail- able alternative is less than the incremental value delivered. Value is a promise that requires substantiation.

In performance-based pricing, prices are adjusted based on product performance or customer outcomes. Providers in a number of indus- tries, including advertising, capital goods, child care, construction, de- fence contracting, education, healthcare, IT, management consultancy, logistics and transportation, social services, and outsourcing, employ variants of performance-based pricing. For a literature review, see Selviaridis and Wynstra (2015). Performance-based pricing is intuitive- ly appealing since it appears to align interests. In healthcare, the envi- ronment where these arrangements have been studied better than in any other context, recent meta-analyses find that customer benefits in terms of improved quality are mixed and, where positive, moderate at best (Weibel, Rost, & Osterloh, 2010; Weissert & Frederick, 2013). Fur- thermore, evidence for improved cost effectiveness for customers is “lacking” (Eijkenaar, Emmert, Scheppach, & Schöffski, 2013, p. 124).

Performance-based pricing leads to cheating (Gravelle, Sutton, & Ma, 2010), gaming (Koning & Heinrich, 2013), adverse customer selection (Hendrickson, 2008), supplier focus on reaching performance thresh- olds (Hendrickson, 2008), the crowding out of intrinsic motivation (Weibel et al., 2010), perceived injustices due to weak links between ef- forts and results (Eijkenaar et al., 2013), and substantially increased transaction costs (Garrison et al., 2013). Data from industrial procure- ment suggest that performance-based contracting tends to favour suppliers at the detriment of customers under certain conditions (GAO, 2004).

In B2B, where frequently many suppliers work together to deliver value to customers, it may be practically impossible to dis-entangle the specific performance improvements attributable to one specific sup- plier and thus determine the specific performance incentive payable in case more than one supplier opts for performance-based pricing.

Value-based pricing usually does not imply performance-based pric- ing. Nagle, Hogan, and Zale (2011, p. 60) note: “In most cases, however, performance-based pricing [based on customer value] is simply imprac- tical.” Likewise, performance-based pricing does not imply value-based pricing: service-level agreements (SLAs), KPIs, and pay-for-perfor- mance incentives are routinely added to existing pricing mechanisms that are cost- and competition-based.

Two forms occur where value-based pricing and performance pricing intersect. Outcome-based contracting (Ng, Ding, & Yip, 2013) links pay- ments to a set of indicators (Hünerberg & Hüttmann, 2003) that are po- tentially aligned with customer value: input-based contracts (e.g., linked to intensity of use) usually are not, but output-based contracts linked to performance levels (e.g., uptime) and output-based contracts linked to customer economics (e.g., cost savings) usually are. In performance- based risk-sharing agreements (the healthcare industry uses the term “value-based pricing”), suppliers participate in improvements in custom- er-defined outcomes (i.e., upside risk sharing), although they usually do not share the downside risk should customer economics deteriorate as a result of the transaction. True performance-based value-based pricing ar- rangements will require that suppliers share performance upsides and downsides, that is, that suppliers pay their customers for failing to meet defined outcomes. These cases are extremely rare.

For the reasons outlined, the adoption of performance-based risk-shar-ing agreements is slowing in healthcare in favour of simpler arrangements with ex ante pricing (Carlson, Gries, Yeung, Sullivan, & Garrison, 2014).

The current pricing literature thus seems to suggest the following. One: Performance-based pricing is a pseudo-intelligent solution to the misalignment between value and price in competition- or cost-based pricing. Two: Value quantification is especially important in the context of value-based pricing where it aligns buyer and seller interests without the numerous problems of performance-based pricing arrangements.

3. Hypotheses development

This study derives the key hypotheses from the literature. These find- ings are complemented with data from interviews: I select a very small sample of interviewees purposefully so that organizations that have well-developed capabilities in value quantification and, within these or- ganizations, individuals that are heavily involved in quantifying and documenting value to customers, are represented (see Table 1). The sam- ple is unrepresentative; nevertheless, these interviews provide a poten- tially interesting and complementary perspective to the findings from the literature. A transcription agency transcribes the interviews which I send back to interviewees for validation. The full interviews are published subsequently to this study in two edited book volumes (Hinterhuber & Heutger, 2017; Hinterhuber & Kemps, 2017; Hinterhuber & Snelgrove, 2016; Hinterhuber, Snelgrove, & Quancard, 2017).

3.1. Hypothesized researchmodel

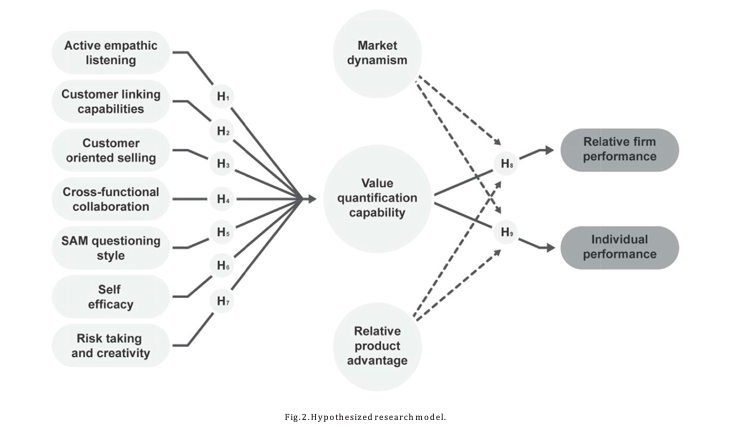

The question of whether core constructs in marketing—market or customer orientation—are psychological traits that shape behaviour or are behaviours that influence psychological traits has vexed the litera- ture for decades (Donavan, Brown, & Mowen, 2004; Narver & Slater, 1998). Recent meta-analytic studies tend to lend more support to the idea that core marketing constructs such as market or customer orienta- tion are observable manifestations of underlying cultural or psycholog- ical differences (Homburg & Pflesser, 2000; Zablah, Franke, Brown, & Bartholomew, 2012): a change in culture or psychological traits drives behavioural changes, not the other way around. This research leads to conceptualizing the value quantification capability as a construct that is influenced by underlying psychological traits.

Furthermore, well-executed case studies (Töytäri & Rajala, 2015; Töytäri et al., 2011) and anecdotal evidence in the managerial literature (Anderson et al., 2006; Anderson et al., 2007) suggest that value quanti- fication capabilities increase firm and sales manager performance. The hypothesized research model therefore takes the form appearing in Fig. 2.

3.2. Antecedents of the value quantification capability

Value quantification requires sales managers to translate value—which is subjective, discovered collaboratively with customers, relative to the customer’s best alternative, expressed in monetary terms, and based on a company’s competitive advantage—into the customer’s language. The literature and the interviews indicate that this translation requires particular skills and attitudes: unbiased listen- ing skills, customer linking skills, ability to put client interests ahead of short-term sales targets, cross-functional collaboration within the firm, attitude towards asking meaningful questions that explore the business impact of solving customer problems, self-confidence, and an entrepreneurial attitude comfortable with risk seeking. Each of these points is discussed in detail below.

3.2.1. One: Active emphatic listening

Value quantification requires that sales managers capture dimen- sions of value that are salient to clients (Töytäri, Rajala, & Alejandro, 2015). Active emphatic listening skills (Drollinger & Comer, 2013; Pelham, 2010) are of paramount importance. Two interviewees (Hinterhuber, Snelgrove, & Quancard, 2017, p. 44; Hinterhuber & Snelgrove, 2016, p. 29) observe:

[The most important capability for value quantification] is the ability to listen instead of the ability to push a product. Some lone wolves, some big sales people, will be terrible account managers because they do not listen. … Active listening is active only when you listen to things at very low noise levels: listening to some of the things the cus- tomer tells you that do not seem important, but are very important. So, when the plant manager out there was telling me, “Well, you know, I have a couple of 15-year-old transformers; they leak energy, but that is not a problem. They are not active.” It is a problem. It’s a lot of the customer’s energy bill going down the drain, just like that.

Listening to the low-noise things, capturing those things, is what we call active listening. Active listeners are a rare commodity, especially among salespeople. Salespeople are hunters, they jump at you, they don’t listen. They want to sell, they want to push the product. So, active listening is number one. [Quancard, Former SVP and Head of Global Strategic Accounts,Schneider Electric]

Another unintended learning [in the process of value quantification] came from the old adage we all should know, “listen to your cus- tomers”: they can help you find even more value [in] your offering than you realize. Over the years I′ve improved our value quantifica- tion tool, by having customers challenge me on the benefits included and ask why something was not listed. [Snelgrove, Global VP Value, SKF]

3.2.2. Two: Customer linking capabilities

Value is always co-created with customers (Grönroos & Voima, 2013). Value quantification rests on the abilities to understand cus- tomer needs and to build appropriate relationships with customers (Hooley, Greenley, Cadogan, & Fahy, 2005). When asked about the most important personal characteristics required for effective value quantification, one interviewee comments (Hinterhuber & Kemps, 2017, p. 171):

Crucial—and this is rule number one—is being aligned with the cus- tomer. You’ve got very transactional customers for whom you need somebody who’s really good at project managing and sales pursuits, in order to be able to standardize and industrialize these responses.

… So, to summarize, the number one point is that you need to align the right team with the customer’s culture. Then you will be success- ful internally and externally. [Kemps, Global Sales Director, DHL]

3.2.3 Three: A genuine customerorientation

Value quantification requires that value be defined in accordance with the customer’s best interests, even if doing so is harmful to short-term sales targets. The customer comes first, sales objectives second. Sales managers need to exhibit a customer-oriented ap- proach to selling, as opposed to a hard selling tactic (Schwepker & Good, 2012). One interviewee comments (Hinterhuber & Kemps, 2017, p. 164):

We have developed lots of packaging solutions now in automo- tive that are enabling us to really go in and say: “You should take this. We are not talking about the 4.5 million that your transport is going to cost, because you need 100 runs, we can tell you are only going to need 70 runs, it’s not going to be 4.5 million, it’s go- ing to be 3.8 million.” That’s the type of discussion we can then have. [Selling less than what we could is] a sacrifice you have to make and it’s not always an easy discussion.

When probed about whether he would care less about short-term revenue losses and more about building consultative or collaborative re- lationship with customers, this interviewee responds:

Exactly. … You can either invest in always becoming cheaper and cheaper or you can invest in building up a meaningful relationship. [Kemps, Global Sales Director, DHL]

3.2.4. Four: Cross-functional collaboration

Pricing requires collaboration between different departments within the firm (Lancioni, 2005; Lancioni, Schau, & Smith, 2005). Quantified value propositions are integrating devices that synthesize dispersed knowledge and make it accessible for customers (Wouters & Kirchberger, 2015). Cross-functional collaboration is vital. One of the interviewees observes (Hinterhuber, Snelgrove, & Quancard, 2017, p. 45):

[A key requirement for value creation and quantification] is the abil- ity to collaborate with multi-stakeholders at the customer inside your own company. But again, pure salespeople are very often lone people. They’re lone wolves, as we say. They don’t collaborate. They’re unable to motivate multifunctional teams. There’s no value creation if you’re by yourself—a lone wolf. Value creation is impossi- ble. Value creation is common at the intersections. Value creation re- quires the ability to interpret weak signals. Value creation will come at the intersections of things, intersections of technology, intersec- tions of the customer’s issues, whatever they are. So, the ability to work with multi-stakeholders is the second key characteristic of a good value creator and a good value quantifier.

Quancard, Former SVP and Head of Global Strategic Accounts, Schneider Electric]

These considerations lead to the following set of hypotheses.

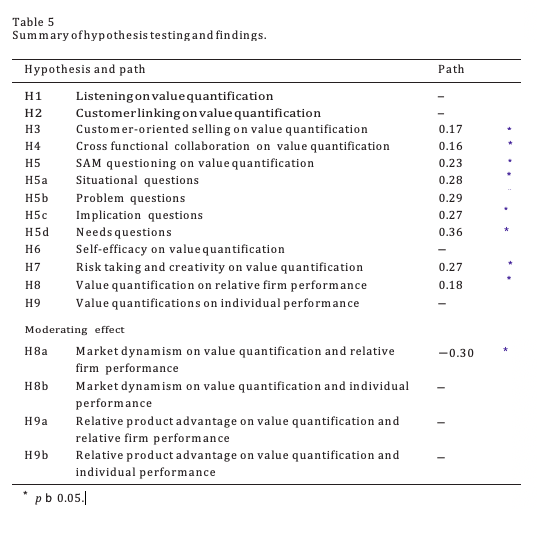

H1. The higher active emphatic listening skills, the higher the value quantification capability.

H2. The higher customer linking capabilities, the higher the value quan- tification capability.

H3. The higher customer-oriented selling skills, the higher the value quantification capability.

H4. The higher the cross-functional collaboration, the higher the value quantification capability.

3.2.5. Five: Value-based selling and value quantification depend on specific selling strategies that sales managers employ

Specifically, the hugely influential literature on SPIN selling – the ac- ronym stands for situation, problem, implication and need-payoff ques- tions – argues that the type of questions that industrial sales managers ask substantially affects sales closure rates (Rackham, 1988). At its core, Rackham argues that less effective sales managers predominantly ask questions exploring the customer’s current situation and current problems. Highly effective sales managers, by contrast, additionally ask questions that explore the impact of customer problems on custom- er operations and, most importantly, the financial impact of solving cus- tomer problems on customer profitability or other key customer metrics.

Because implication and need-payoff questions are aimed at uncovering the financial benefits of solving customer problems, the effect of implication and need-payoff questions on the value quantification capability is expected to be stronger than the effect of situation and problem questions on this capability. The next set of thypotheses concerns the relationship between sales manager questioning style and the value quantification capability.

H5a. The higher the number of situation questions, the higher the value quantification capability.

H5b. The higher the number of problem questions, the higher the value quantification capability.

H5c. The higher the number of implication questions, the higher they value quantification capability.

H5d. The higher the number of need-payoff questions, the higher the value quantification capability.

3.2.6. Six: Self – confidence

Carlos Tavares, CEO of Peugeot, says: “The Peugeot 308 was the Eu- ropean Car of the Year in 2014. But the car was being discounted at a level that wasn’t consistent with the quality of similar cars and com- pared with our German competitors. There was no reason we couldn’t price higher. There was some lack of confidence in our capability” (Chow, 2015). Setting prices based on customer value requires confi- dence (Liozu, 2015). This holds also for value quantification. Thus the next hypothesis is:

H6. The higher the self-efficacy of the sales manager, the higher the value quantification capability.

3.2.7. Seven: Risktaking and creativity

Current research indicates that decision makers in industrial markets may favour cost-based over value-based pricing strategies since the former are perceived to involve less risk than the latter (Hunt & Forman, 2006). Value quantification requires a high toler- ance for ambiguity and uncertainty: costs are objective, value is sub- jective. Buying and selling on value exposes both sellers and buyers to risk (Töytäri et al., 2015). The data from the interviews also suggest that a certain entrepreneurial orientation is beneficial in the context of value quantification. One interviewee observes (Hinterhuber & Heutger, 2017, p. 157):

Sales managers need to be at least dynamic and interested in explor- ing new ideas, however you want to call it. It is… about being pro-ac- tive, being open and being dynamic or thinking about different ways of doing things.

[Heutger, SVP Strategy and Marketing, DHL]

This is hypothesized formally as follows.

H7. The higher risk taking and creativity, the higher the sales manager value quantification capability.

In sum, the data at hand suggest that value quantification capabil- ities are a complex set of attitudes and skills that require sales man- agers to balance potentially opposing traits: the ability to put themselves in the shoes of customers to understand their emotions, motives, and cognitions (H1); trustworthiness to build meaningful relationships (H2); a willingness to put customer interests first and to forgo short-term revenue gains (H3); political savvy and cross- functional coordination skills (H4); business acumen and the ability to ask questions that explore meaningful dimensions of value (H5); self-confidence (H6); and a preference for risk and an entrepreneur- ial attitude (H7). Which of these traits is most relevant for value quantification is a question that the quantitative study is designed to answer.

3.3 Consequences of the value quantification capability

Sales managers quantify value for a reason—to drive performance.

The next set of hypotheses is.

H8. There is a positive relationship between sales manager value quan- tification capability and relative firm performance.

H9. There is a positive relationship between sales manager value quan- tification capability and individual performance.

Do value quantification capabilities always improve performance? Current research (Ingenbleek, Debruyne, Frambach, & Verhallen, 2003; Ingenbleek, Frambach, & Verhallen, 2013) indicates that perfor- mance benefits are contingent on two factors: market dynamism and relative product advantage. The data at hand support this assertion. To the question “When does value quantification not work?” an interview- ee (Hinterhuber, Snelgrove, & Quancard, 2017, p. 47) responds (see also Section 1):

It might be when a product is very commoditized. It might be that competitors copy you very quickly. Whatever value you bring, in logistics or whatever—take the examples we discussed before [. .] it depends on how quickly your competitors catch up. If your competitors catch up very quickly, , then it’s really, re- ally difficult.

I would look at it more from a competitive standpoint than from an industry perspective alone. I do not believe there is a specific industrial sector. So, I think the lack of value quantification is about the competitive environment more than anything else.

[Quancard, Former SVP and Head of Global Strategic Accounts, Schneider Electric] The next set of hypotheses is therefore as follows.

H8a. Market dynamism negatively moderates the relationship be- tween value quantification capability and relative firm performance such that, for high competitive intensity, the relationship is weaker than for low competitive intensity.

H8b. Market dynamism negatively moderates the relationship be- tween value quantification capability and individual sales manager per- formance such that, for high market dynamism, the relationship is weaker than for low market dynamism.

H9a. Product advantage positively moderates the relationship between value quantification capability and relative firm performance such that, for high product advantage, the relationship is stronger than for low product advantage.

H9b. Product advantage positively moderates the relationship between value quantification capability and individual sales manager performance such that, for high product advantage, the relationship is stronger than for low product advantage.

4. Methods

4.1. Data collection and sampling

The dataset consists of an e-mail list of US sales and account man- agers purchased from a commercial database provider. Respondents are contacted in three waves starting in January 2014. From 2904 recip- ients I receive 246 partially or fully completed questionnaires for a response rate of 8%—similar to the response rate for other B2B pricing studies (Homburg, Allmann, & Klarmann, 2014; Liozu, 2015).

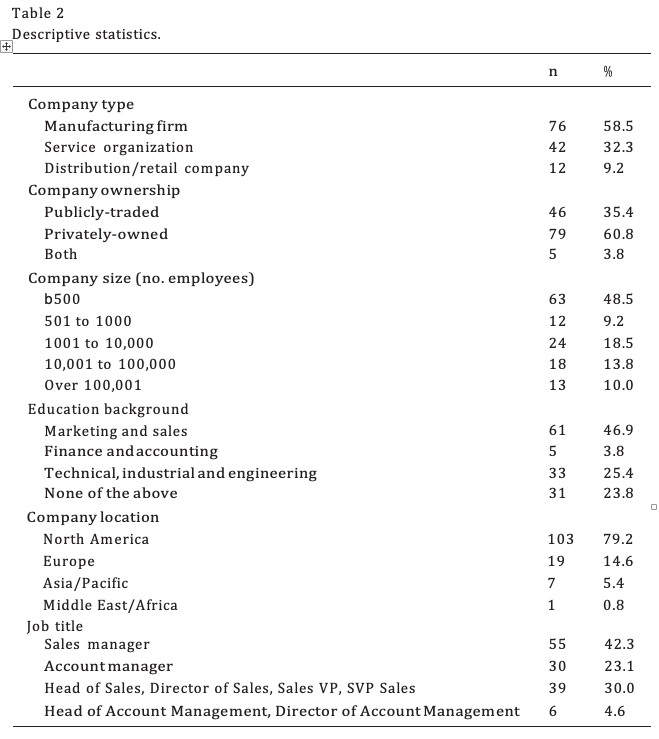

To ensure exclusive participation of B2B sales and account managers, I build in a filter question asking respondents to confirm their job titles (i.e., sales manager/account manager) and a filter question asking re- spondents about the main line of business of their companies (B2B/ B2C). After eliminating incomplete responses or responses from un- qualified candidates, I retain 131 questionnaires from B2B sales or account managers for final analysis. Table 2 provides the descriptive information for the sample: Respondent companies are typically indus- trial manufacturing firms that are privately owned, headquartered in the US with N 500 employees.

4.2 Measuredevelopmentandassessment

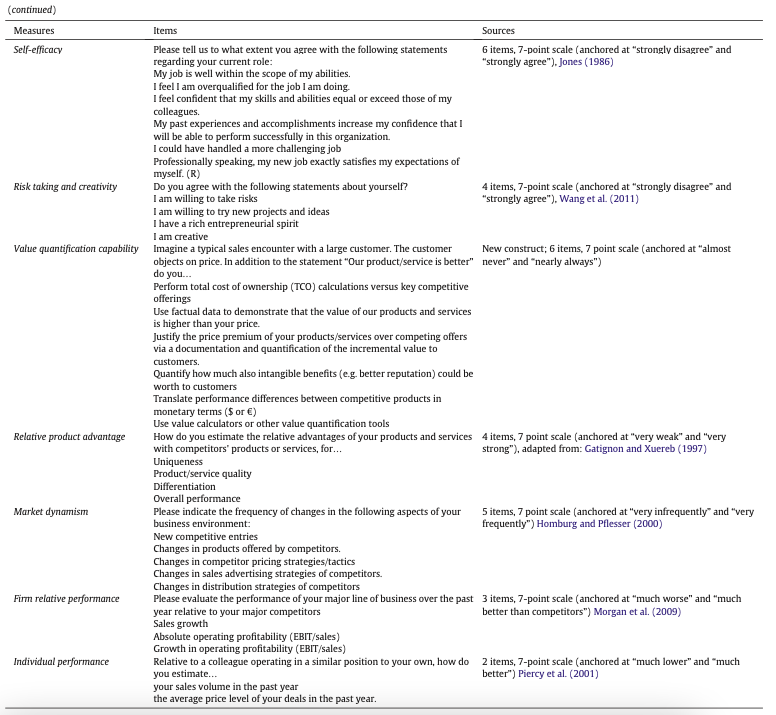

I take all scales from the current literature and develop a new scale to measure the value quantification capability. I assess content and face va- lidity through a full review of the literature to ensure that measurement items cover the domain of the constructs (Churchill, 1979; Nunnally, 1978). Measures, items, and sources are in Appendix A.

4.2.1 Independentvariables

4.2.1.1. Activeemphaticlistening. Active emphatic listening is based on a multi-dimensional approach to listening that involves sensing, process- ing, and responding to customer words, ideas, feelings, and positions. The five-item scale is from Drollinger and Comer (2013).

4.2.1.2. Customer linking capabilities. Customer linking capabilities are among the most important market-based resources of any organization (Day, 1994). They include the ability to identify customer needs togeth- er with the capabilities to build effective customer relationships. The five-item scale is from Hooley et al. (2005).

4.2.1.3. Customer-orientedselling.The selling-orientation customer-ori- entation (SOCO) scale measures the customer orientation of sales man- agers at the individual customer level. The construct measures sales managers’ desire to help customers, assess their specific needs, offer sat- isfactory products, and adequately describe their products, as well as sales managers’ reluctance to engage in deceptive or hard selling prac- tices (Periatt, LeMay, & Chakrabarty, 2004). The 10-item scale is from Periatt et al. (2004).

4.2.1.4. Cross-functional collaboration. Cross-functional collaboration measures inter-functional collaboration between sales and other de- partments, such as marketing, management, and sales support. The seven-item scale is from Rodriguez and Honeycutt (2011).

4.2.1.5. Salesmanagerquestioningstyle.The scale is new and based on the SPIN selling questions (Rackham, 1988). The extent of engagement with each of the four different questioning styles is measured with four sin- gle-item measures, anchored at “does not apply” and “fully applies.” The use of a single-item scale to measure each of these different questioning styles is warranted in this case (Bergkvist & Rossiter, 2007; Sackett & Larson, 1990).

4.2.1.6. Self-efficacy. The self-efficacy scale measures confidence. Self- efficacy is positively related to challenging personal goals and job performance (Brown, Jones, & Leigh, 2005). Self-efficacy refers to individuals’ beliefs that they possess the skills and resources necessary to succeed at a given task. The six-item scale is from Jones (1986).

4.2.1.7. Risk taking and creativity. This risk-taking and creativity scale measures willingness to take risks, willingness to try new ideas, creativ- ity, and entrepreneurial orientation at the individual level. The four- item scale is from Wang, Tsui, and Xin (2011).

4.2.1.8. Value quantification capability. Since there is no empirical precedent to measure the value quantification capability, I develop a multiple item scale. The construct measures the ability of the sales manager to translate product or service features into quantified customer value where customer value has both a quantitative (financial) and a qualita- tive (intangible) component. The scale has six items.

4.2.2 Moderators

4.2.2.1. Market dynamism. The market dynamism scale measures the speed of change in the external competitive environment. The five item scale is adapted from Homburg and Pflesser (2000).

4.2.2.2. Relativeproductadvantage.The relative product advantage scale measures product differentiation vis-à-vis competitors. This four-item scale is from Gatignon and Xuereb (1997).

4.2.3.1. Firmrelativeperformance.This scale measures the perceived firm performance relative to key competitors. This is thus a subjective evalu- ation of firm performance. The decision to use relative firm performance is warranted in samples that have a potentially high number of small and medium-sized companies where objective performance indicators frequently are distorted (Sapienza, Smith, & Gannon, 1988; Simsek, 2007; Simsek, Veiga, Lubatkin, & Dino, 2005). Subjective performance measurement is reliable (Kumar, Jones, Venkatesan, & Leone, 2011). This three-item scale is adapted from Morgan, Vorhies, and Mason (2009).

4.2.3.2. Individual performance. The sales manager individual perfor- mance scale measures the sales volume and price levels achieved at the individual level relative to a colleague operating in a similar posi- tion. This two-item scale is adapted from Piercy, Cravens, and Lane (2001).

4.3. Non-responsebias

In order to evaluate any potential response bias, I categorize partici- pants into two groups: those completing the survey within 2 weeks (n = 59; 24%) and those completing after (n = 187; 76%). Due to dis- crepancies in group size, potential differences in outcome by response date are tested using non-parametric Mann-Whitney U tests. There are no significant differences across any items, ps N 0.05, suggesting that individuals’ responses do not appear to be impacted by early versus late responses.

5. Results

To evaluate the theorized models examining the link between indi- vidual factors on value quantification capability and the impact of value quantification on performance measures, I utilize partial least square structural equation modeling (PLS-SEM) with SmartPLS v.3.2. I choose PLS-SEM instead of traditional, covariance-based SEM (CB-SEM) for two main reasons. First, thanks to fewer data restrictions and higher model flexibility, PLS is preferable for exploratory research where mea- sures are not yet fully established (Echambadi, Campbell, & Agarwal, 2006). Second, PLS-SEM models are more robust than CB-SEM at exam- ining complex relationships between latent variables with relatively small sample sizes (Anderson & Gerbing, 1988; Hair, Sarstedt, Ringle, & Mena, 2012).

In PLS-SEM, path coefficients indicate the absolute magnitude of di- rect and indirect effects between latent constructs. Path coefficients are interpreted as follows: |~ 0.10| indicates a small effect, |~0.30| indicates a moderate effect, and |N 0.50| indicates a large effect.

Model evaluation occurs in three stages. The first stage of analysis consists in assessing the measurement quality and ensuring appropriate psychometric properties of the items chosen. Next, the relative weights are calculated using a path weighting scheme and a maximum of 300 it- erations. Significance of these paths is assessed by bootstrapping of 500 samples with no sign changes. Weak and non-significant paths are re- moved to increase the parsimony of the final model. Of note, PLS- based approaches to SEM do not evaluate goodness of fit of the model in a way analogous to CB-SEM; rather, the evaluation of the quality of the model is assessed through examination of paths, significance, and the measurement quality. Effect size and magnitudes of the final model are assessed through the path coefficients as well as the observed R2 values.

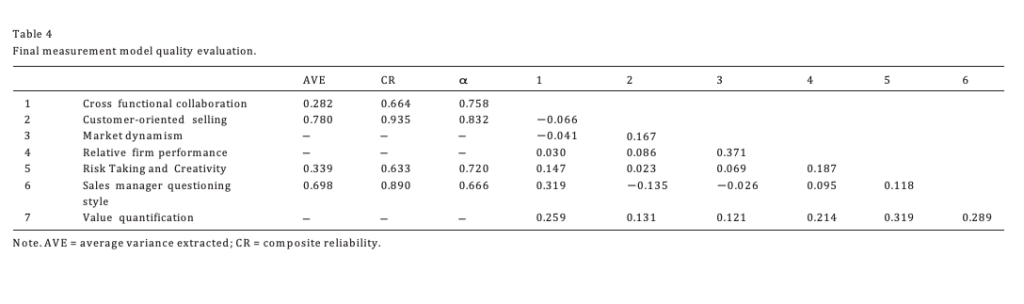

5.1. Measurement model quality assessment

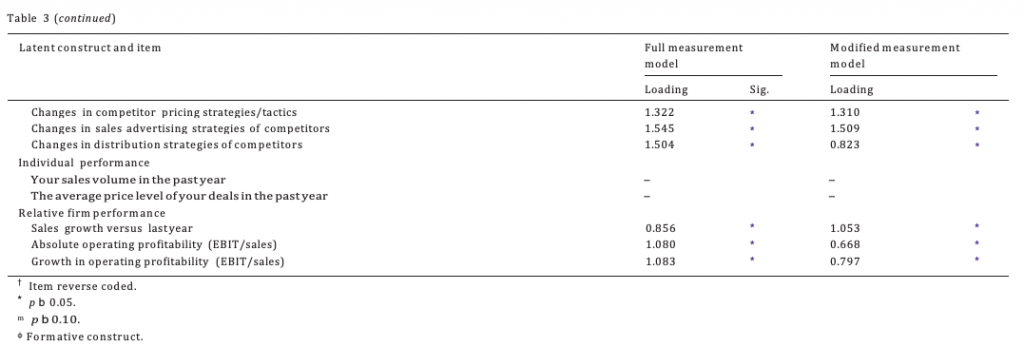

Prior to testing the theorized model, I examine the measurement model: Table 2 provides an overview of the full and modified measure- ment model. Following initial investigation of the measurement model, I remove items and constructs with weak and/or non-significant outer loadings to improve the overall quality of the measurement model. This step leads to the removal of the following latent constructs: active empathetic listening, customer linking capabilities, and self-efficacy. Additionally, due to high multicollinearity between individual perfor- mance items, I test the measurement model using each indicator sepa- rately; however, this construct is not significantly related to any of the remaining constructs in the model and is, as such, removed from the model (see Table 3).

Following removal of poorly performing items and constructs, I find

that the outer loadings across latent variables are significant or ap- proaching significance (e.g., pb 0.10). While some weak outer loadings are observed, these items are retained in the model for theoretically driven reasons to ensure that these important facets can be accounted for in the structural model. Additionally, there are some outer loadings that exceed the typical constraint value of 1.00, which may indicate some degree of multicollinearity between indicators of the same latent constructs; however, examination of other metrics (e.g., average vari- ance extracted [AVE], reliability indices) suggests that this is not prob- lematic for the factor structure and, as such, outer loadings N 1 are retained in the measurement model.

Additionally, the AVE, composite reliability (CR), and internal consistency (Cronbach’s α) are evaluated based on the recommendations in the current literature (Fornell & Larcker, 1981; Nunally & Bernstein, 1994). Table 4 provides the data.

Observed AVE values for customer-oriented selling and sales manag- er questioning style are above the desired minimum cut-off value of 0.500 for AVEs. Cross-functional collaboration and risk taking/creativity are below the desired cut-off; however, these are retained in the model as reliability measures, and outer loadings are within the acceptable range.

Composite reliabilities of all latent constructs are all well above the minimum cut-off of 0.60 (Fornell & Larcker, 1981). Additionally, inter- nal consistency, expressed as Cronbach’s alpha, of all latent constructs is in the acceptable to excellent range, αs ranging from 0.666 (questioning style) to 0.832 (customer-oriented selling).

Last, I examine discriminant validity by evaluating the correlations between latent constructs, which indicates that all correlations are below the critical threshold of 0.85, demonstrating that there does not appear to be redundancy in the indicators and the overall model.

5.2. Structural model

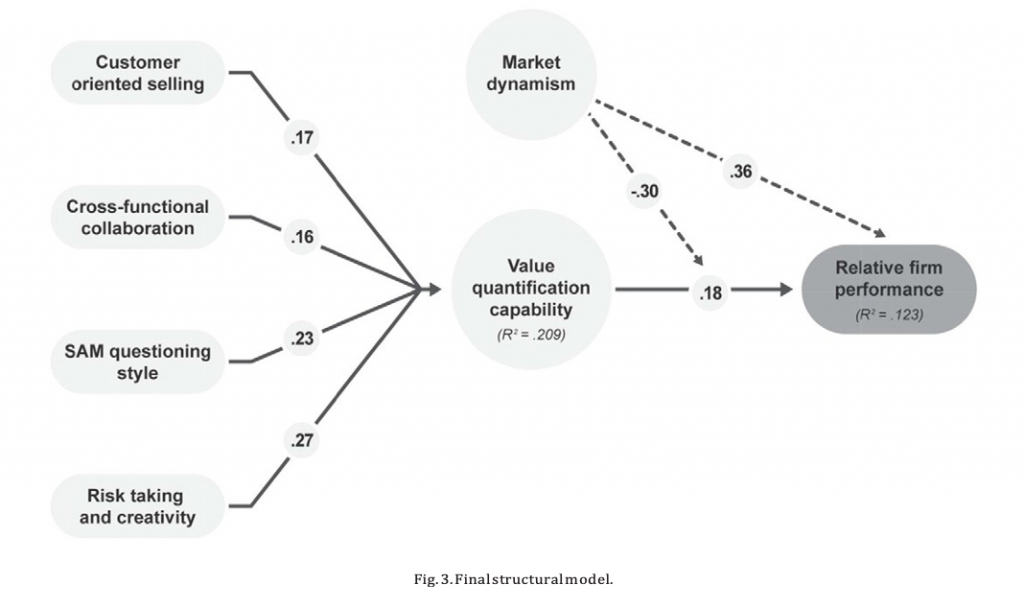

To create the most parsimonious model, I remove non-significant paths and non-meaningful latent constructs. The final structural model is in Fig. 3.

Cross-functional collaboration, customer-oriented selling, sales manager questioning style, and risk taking and creativity are all signifi- cantly and positively associated with the value quantification capability and account for over 20% of the total variance explained (R2 = 0.209). Risk taking and creativity is the strongest indicator of value quantification capability (0.23), followed by questioning style (0.23), customer oriented selling (0.17), and cross functional collaboration (0.16).

On questioning style: All questions collectively are significantly as sociated with value quantification, evidenced by significant path leadings in the full measurement model tested. Asking questions about the payoff of a solution has the strongest weight in overall questioning la- tent scores, followed by asking about consequences, and asking about customer’s problems, difficulties, and dissatisfactions; asking about the current situation has the lowest weight on overall scores.

Furthermore, there is a significant, positive relationship between the value quantification capability and relative firm performance. Value quantification capabilities account for 12.3% of the variance in relative firm performance. The relationship between value quantification capability and individual performance is not significant. However, this relationship cannot be fully tested in the final structural model.

Testing for moderators leads to the following: There is no interaction effect of relative product advantage and value quantification capability on relative firm performance. Relative product advantage is also not sig- nificantly associated with relative firm performance. Therefore, I remove relative product advantage from the model. There is, however, a significant direct effect of market dynamism on relative firm performance. There is also a significant moderating effect of market dynamism on the relationship between value quantification capability and relative firm performance (−0.30), suggesting that when the competitive intensity increases the impact of value quantification capability on relative firm performance decreases. Table 5 provides the details.

6. Discussion

“Customer value is B2B marketing’s defining preoccupation” (Wiersema, 2013, p. 484): the Marketing Science Institute (Marketing Science Institute, 2010, 2014) and the Institute for the Study of Business Markets (ISBM, 2012) both highlight value quantification as a key re- search priority. This study addresses this fundamentally important re- search question and advances what is known about the origins and benefits of value quantification capabilities in industrial markets. After polling 131 US sales and account managers in B2B, this study offers the following four substantial contributions.

First, value quantification capabilities substantially and positively in- fluence firm performance—always. This finding, based on quantitative research, thus corroborates data from qualitative research (Töytäri &

Rajala, 2015) and the managerial literature (Anderson et al., 2006) that value quantification is beneficial. Companies are thus well advised to invest in and nurture value quantification capabilities. These capabil- ities enable sales and account managers to translate competitive advan- tages into quantified customer benefits. Value quantification requires that sales managers go beyond quantifying merely total cost of owner- ship to customers. Value is multi-dimensional: value quantification requires the ability to translate the full spectrum of benefits into one figure representing the economic value that customers receive. The con- struct validity of the new scale, value quantification capability, appears reasonably satisfactory. However, while prior research and the litera- ture suggest that this capability includes the ability to quantify the value of intangible benefits (i.e., qualitative elements), the current data show no such relationship. Further research may be needed to un- derstand the role of qualitative benefits in value quantification.

Second, the positive impact of value quantification capabilities on

firm performance increases under conditions of low market dynamism. In highly volatile markets, value quantification capabilities have a positive, albeit weaker impact on firm performance. Value quantification is highly beneficial when markets are stable. This finding thus extends current research findings: in highly dynamic markets, value quantification still contributes positively to overall firm performance, but less so than in stable markets. In place of value quantification capabilities, there are other capabilities that influence firm performance in highly dynamic markets which future studies should attempt to identify. This study thus resolves the tension that the mixed evidence from practitioners cited in Section 1 as well as the conflicting data from the interviews produced: the benefits of value quantification depend on market characteristics.

Third, the value quantification capability has no positive effect on individual sales manager performance. At first sight, this finding seems counterintuitive. However, the data from the interviews indicate that the relationship between individual value-quantification capability and short-term individual performance is all but straightforward.

Short- term individual performance in B2B is influenced by a number of fac- tors: the fit between the own offer and customer purchase criteria (or, put differently, high current performance is also the result of the ability of sales managers to influence customer purchase criteria in the first place), current economic conditions (recession vs. growth), sales man- ager access at the customer company (procurement vs. decision maker), the stage of the customer in the decision-making process (in- formation gathering vs. final negotiations with qualified suppliers), and the maturity of customers themselves (selection based on price vs. selection based on value). At the organizational level, these factors seem to balance out, but at the level of individual sales managers, a high level of value quantification capability does not automatically lead to immediate superior performance. The factors mentioned are moderators that could influence the strength of the relationship between the individual value quantification capability and individual performance. One interviewee, for example, comments on the performance benefits of value quantification (Hinterhuber & Kemps, 2017, p. 173):

So yes, that’s why simply—in Japan they say, there is a beautiful ex- pression, they call it, “You have to be prepared to sit on a rock for three years,” which means that sometimes you just kind of have to be in a difficult painful situation before you get results, and fortunately—I know that’s difficult for many of my colleagues, but fortunately I′m in an organization where that is understood that things may take time and that it’s accepted that you need to some- times make a significant investment to service that customer in or- der to achieve a longer term sustainable success, and I′m very well aware that that’s not the case in all organizations.

[Kemps, Global Sales Director, DHL]

Selling is complex (Franke & Park, 2006). At the level of the individual sales manager, the model presented here does not find that the value quantification capability translates to superior short-term performace that is, sales. The data in this study thus raise the question of of what superior sales manager performance actually is. Superior performance at the individual level could be, as the interviewee suggested “waiting,” in other words, relationship building, value verification, customer-supporting activities, information gathering—and not selling. Future studies thus should expand on the idea of defining sales manager performance and could subsequently attempt to include a broader set of factors that examine under which conditions individual value- quantification capabilities improve individual performance.

Fourth, this study examines the individual-level antecedents of the value quantification capability. The data in this study indicate that four factors are positively associated with value quantification capability: risk taking and creativity, sales manager questioning style, customer- oriented sales, and cross-functional collaboration. Value is subjective and uncertain: risk-seeking behaviour and an entrepreneurial attitude are beneficial for value quantification. Value quantification requires the ability to understand the business impact of the products or services offered: SPIN selling (Rackham, 1988), only apparently an old dog, is beneficial: value quantification capabilities are highest in sales man- agers who predominantly ask implication and need-payoff questions. Financial acumen, rather than the more-generic active emphatic listen- ing skills, is thus critically important for value quantification. Sales managers thus need to possess the insight, intelligence, and customer knowledge necessary to ask meaningful questions that explore the fi- nancial consequences of the value proposition. A genuine customer ori- entation is furthermore beneficial for value quantification capability: understanding customer needs and a willingness not to sell unless in the customer’s own best interest are salient aspects of this ability. This unwillingness to sell unless in the customer’s best interest may partly explain the absence of a direct relationship between value quantifica- tion capability and individual performance. Value quantification finally requires cross-functional collaboration: sales managers need to liaise with different stakeholders in order to synthesize and integrate how dif- ferent departments within the firm create financial value for customers.

The following picture emerges at the level of micro-foundations of the value quantification capability: an entrepreneurial, risk-seeking in- dividual with a high level of financial acumen, exhibiting a genuine cus- tomer orientation that puts understanding ahead of selling, and an ability to coordinate different functions internally emerge as behaviour- al traits that enable the formation of the value quantification capability at the level of individual sales and account managers.

7. Implications for B2B marketing practice and theory

This study has important implications for B2B marketing practice. Value quantification capabilities at the level of sales and account managers matter, and for all products and under all environmental conditions: value quantification capabilities always improve overall firm performance. Under conditions of high market dynamism, value quanti-fication capabilities are still beneficial, but less so than in stable markets. This finding implies that companies are well advised to invest in developing sales and account manager value-quantification capabilities regardless of whether they sell (apparent) commodities or highly differ- entiated products and regardless of whether they operate in stable or highly dynamic markets. Value quantification capabilities are always beneficial and especially so when markets are relatively stable.

The data indicate that value quantification capabilities do not lead to higher individual performance: short-term individual performance is influenced by other factors not examined in detail herein. This study also suggests avenues to develop value quantification capabilities at the level of individual sales and account managers. Encouraging risk taking, experimentation, fostering creativity and crossfunctional collaboration, educating sales managers to ask the right questions during the sales encounter—that is, implication and need payoff questions and championing a true customer orientation that puts customer needs ahead of short-run revenue realization are measures that senior executives in B2B can and should implement to develop value quantification capabilities within their organization.

To senior executives, this study can further provide guidance in hir- ing and promotion decisions: in many companies there probably are customers or sales territories where value quantification is critically im- portant, either because customers negotiate aggressively (Wieseke, Alavi, & Habel, 2014) or because customers themselves demand a quan- tified value proposition (Ernst & Young, 2002). The behavioral traits that this study identifies—risk taking and creativity or SPIN questioning style, for example can be used to identify the most suitable sales managers and allocate them to customers where these value quantification capabilities are needed most.

This study also contributes significantly to B2B marketing theory. The study identifies a new construct, value quantification capability, as an important, albeit hitherto unexamined, antecedent of firm perfor- mance in B2B markets. Value quantification capabilities are elements of value-based selling capabilities (Terho et al., 2012) or, more generally, of salesforce capabilities (Guenzi, Sajtos, & Troilo, 2016), and future studies could examine the relative contribution of these capabilities to sales performance vis-à-vis other, related capabilities, such as customer insight generation, market opportunity identification, offer development, pricing, sales negotiation, or offer delivery capabilities.

By identifying a moderator, this study provides a rich and nuanced picture of the role of value quantification capabilities in industrial mar- kets. It also sheds light on the individual-level micro-foundations of the capability to quantify value in B2B and thus suggests the existence of a link between psychological traits and behaviours at the individual level and outcomes at the level of the firm.

The examination of micro-foundations of marketing strategy is a particular fruitful research domain: some desirable activities and capa- bilities may be difficult to observe in practice; an understanding of their micro-level foundations allows researchers and managers to iden- tify relevant proxies for such behaviours and capabilities (Storbacka, Brodie, Böhmann, Maglio, & Nenonen, 2016). Current research identifies links between these micro-foundations, such as thinking styles or per- sonality types, and sales performance (Fraenkel, Haftor, & Pashkevich, 2016; Groza, Locander, & Howlett, 2016; Lussier & Hartmann, 2017); re- search on the micro-foundations of marketing capabilities is, however, still in its infancy, and this study aims to contribute to research in this emerging domain.

This study also points towards future studies that are needed to enhance the understanding of the benefits and the limits of value quantification in industrial markets: given the explorative nature of the present study, more research is warranted to broaden the understand- ing of value quantification capabilities and their importance in contexts that are dynamic: value cocreation processes, new product innovation, or new customer acquisition and the role of value quantification capabilities therefore appear as fertile research grounds.

8. Limitations

This study has limitations: at a fundamental level, the ability to quantify value has to be raised. The great economist Alfred Marshall (1925, p. 422) wrote over a century ago:

In my view every economic fact, whether or not it is of such a nature as to be expressed in numbers, stands in relation as cause and effect to many other facts: and since it never happens that all of them can be expressed in numbers, the application of exact mathematical methods to those which can, is nearly always a waste of time, while in the large majority of cases it is positively misleading; and the world would have been further on its way forward if the work had never been done at all.

Applied to the mundane topic of value quantification, these words thus at least suggest that more research is needed to explore, to cite an example, the relationship between ex-ante value quantification and ex-post value verification. Also here, individual characteristics of sales and account managers could play a role.

Further limitations relate to the response rate, sample size, and mea- surement model. To address these limitations, the current study should be replicated with a larger sample and using a CB-SEM approach to bet- ter examine these relationships and the psychometric properties of the research model. Furthermore, it is expected that CB-SEM approaches will be better able to address potential issues of multicollinearity and that more latent constructs will be able to be retained in the final structural models. Additionally, the current study and PLS-SEM methods could control for potential covariate ways. Further covari- ance-based models may be needed to examine the impact that firm-level factors may have on the relationships described in this study.

Finally, future studies should apply configurational theory (Isaksson & Woodside, 2016; Woodside, 2015a; Woodside, 2016), as opposed to variable-based approaches, to the study of value quan tification. Fuzzy-set qualitative comparative analysis (Ordanini, Parasuraman, & Rubera, 2013; Woodside, 2015b) appears particularly promising.

Acknowledgements

The author wishes to thank the following individuals for their contributions to the present study: Evandro Pollono (data collec-

Appendix A. Constructs and scales.

tion), John Maddox (data analysis), Candi Wong (graphics), Kristen Ebert-Wagner (editing). In addition, two reviewers and Arch Woodside contributed substantially towards improving the present paper.

References

Adade, M., & Simonetti, A. (2013). The collection – Examples of true excellence in marketing and sales at DSM, DSM internal publication. The Netherlands: Heerlen.

Anderson, J. C., & Gerbing, D. W. (1988). Structural equation modeling in practice: A re- view and recommended two-step approach. Psychological Bulletin, 103(3), 411–423.

Anderson, J. C., Narus, J. A., & Van Rossum, W. (2006). Customer value propositions in business markets. Harvard Business Review, 84(3), 90.

Anderson, J., Kumar, N., & Narus, J. (2007). Value merchants: Demonstrating and documenting superior value in business markets. Boston, MA: Harvard Business School Press.

Anderson, J., Narus, J., & Narayandas, D. (2008). Business market management: Understand- ing, creating, and delivering value (3rd ed.). Upper Saddle River, NJ.: Prentice Hall.

Bergkvist, L., & Rossiter, J. R. (2007). The predictive validity of multiple-item versus single- item measures of the same constructs. Journal of Marketing Research, 44(2), 175–184. Brown, S. P., Jones, E., & Leigh, T. W. (2005). The attenuating effect of role overload on re- lationships linking self-efficacy and goal level to work performance. Journal of Applied

Carlson, J. J., Gries, K. S., Yeung, K., Sullivan, S. D., & Garrison, L. P., Jr. (2014). Current status and trends in performance-based risk-sharing arrangements between healthcarepayers and medical product manufacturers. Applied Health Economics and HealthPolicy, 12(3), 231–238.

Chow, J. (2015, 17 March). Peugeot CEO uses cost cuts to turn corner on profitability. The Wall Street Journal.

Churchill, G. A., Jr. (1979). A paradigm for developing better measures of marketing con- structs. Journal of Marketing Research, 16(1), 64–73.

Day, G. (1994). The capabilities of market-driven organizations. Journal of Marketing, 58(4), 37–52.

Dolan, R. J. (1996). Black & Decker Corporation: Power tools division – video supplement (HBS product #: 596510-VID-ENG). Boston, MA: Harvard Business School.

Dolan, R. J. (1998). Black & Decker Corporation: Power tools division – teaching note (HBS case no 5–598-106) Boston, MA: Harvard Business School.

Donavan, D. T., Brown, T. J., & Mowen, J. C. (2004). Internal benefits of service-worker cus- tomer orientation: Job satisfaction, commitment, and organizational citizenship be- haviors. Journal of Marketing, 68(1), 128–146.

Drollinger, T., & Comer, L. B. (2013). Salesperson’s listening ability as an antecedent to re- lationship selling. Journal of Business & Industrial Marketing, 28(1), 50–59.

Echambadi, R., Campbell, B., & Agarwal, R. (2006). Encouraging best practice in quantita- tive management research: An incomplete list of opportunities. Journal of Management Studies, 43(8), 1801–1820.

Eijkenaar, F., Emmert, M., Scheppach, M., & Schöffski, O. (2013). Effects of pay for perfor- mance in health care: A systematic review of systematic reviews. Health Policy, 110(2), 115–130.

Ernst, & Young (2002). Fortune 1000 IT buyer survey: What could shorten sales cycles and further increase win rates for technology vendors? Economics & Business Analytics white paper.

Fornell, C., & Larcker, D. F. (1981). Evaluating structural equation models with unobserv- able variables and measurement error. Journal of Marketing Research, 18(1), 39–50.

Fraenkel, S., Haftor, D. M., & Pashkevich, N. (2016). Salesforce management factors for successful new product launch. Journal of Business Research, 69(11), 5053–5058.

Franke, G. R., & Park, J. -E. (2006). Salesperson adaptive selling behavior and customer ori- entation: A meta-analysis. Journal of Marketing Research, 43(4), 693–702.

GAO (2004). Defense Management – Opportunities to Enhance the Implementation of Perfor- mance-Based Logistics, United States Government Accountability Office, GAO-04-715. Washington, D.C.

Garrison, L. P., Towse, A., Briggs, A., De Pouvourville, G., Grueger, J., Mohr, P. E., … Sleeper,

M. (2013). Performance-based risk-sharing arrangements – Good practices for design, implementation, and evaluation: Report of the ISPOR good practices for perfor- mance-based risk-sharing arrangements task force. Value inHealth, 16(5), 703–719.

Gatignon, H., & Xuereb, J. -M. (1997). Strategic orientation of the firm and new product performance. Journal of Marketing Research, 37(1), 77–90.

Gravelle, H., Sutton, M., & Ma, A. (2010). Doctor behaviour under a pay for performance contract: Treating, cheating and case finding? The Economic Journal, 120(542), 129–156.

Grönroos, C., & Voima, P. (2013). Critical service logic: Making sense of value creation and co-creation. Journal of the Academy of Marketing Science, 41(2), 133–150.

Groza, M. D., Locander, D. A., & Howlett, C. H. (2016). Linking thinking styles to sales per- formance: The importance of creativity and subjective knowledge. Journal of Business Research, 69(10), 4185–4193.

Guenzi, P., Sajtos, L., & Troilo, G. (2016). The dual mechanism of sales capabilities in influencing organizational performance. Journal of Business Research, 69(9), 3707–3713.

Haas, A., Snehota, I., & Corsaro, D. (2012). Creating value in business relationships: The role of sales. Industrial Marketing Management, 41(1), 94–105.

Hair, J. F., Sarstedt, M., Ringle, C. M., & Mena, J. A. (2012). An assessment of the use of par- tial least squares structural equation modeling in marketing research. Journal of the Academy of Marketing Science, 40(3), 414–433.

Hendrickson, M. A. (2008). Pay for performance and medical professionalism. Quality Management in Healthcare, 17(1), 9–18.

Hinterhuber, A. (2004). Towards value-based pricing—An integrative framework for deci- sion making. Industrial Marketing Management, 33(8), 765–778.

Hinterhuber, A. (2008). Customer value-based pricing strategies: Why companies resist.

Journal of Business Strategy, 29(4), 41–50.

Hinterhuber, A., & Heutger, M. (2017). Interview: Implementing value quantification in B2B. In A. Hinterhuber, & T. Snelgrove (Eds.), Value first, then price: Quantifying value in business markets from the perspective of both buyers and sellers (pp. 153–160). Milton Park, UK: Routledge.

Hinterhuber, A., & Kemps, P. (2017). Interview: The ring of truth – Value quantification in B2B services. In A. Hinterhuber, & T. Snelgrove (Eds.), Value first, then price: Quantify- ing value in business markets from the perspective of both buyers and sellers (pp. 161–177). Milton Park, UK: Routledge.

Hinterhuber, A., & Snelgrove, T. (2016). Interview with an expert: Mr. Todd Snelgrove, Chief Value Officer, SKF. In A. Hinterhuber, & S. Liozu (Eds.), Pricing and the sales force (pp. 24–29). Milton Park, UK: Routledge.

Hinterhuber, A., Snelgrove, T., & Quancard, B. (2017). Interview: Nurturing value quanti- fication capabilities in strategic account managers. In A. Hinterhuber, & T. Snelgrove (Eds.), Value first, then price: Quantifying value in businessmarkets from the perspective of both buyers and sellers (pp. 39–48). Milton Park, UK.: Routledge.

Homburg, C., & Pflesser, C. (2000). A multiple-layer model of market-oriented organiza- tional culture: Measurement issues and performance outcomes. Journal of Marketing Research, 37(4), 449–462.

Homburg, C., Allmann, J., & Klarmann, M. (2014). Internal and external price search in in- dustrial buying: The moderating role of customer satisfaction. Journal of Business Research, 67(8), 1581–1588.

Hooley, G. J., Greenley, G. E., Cadogan, J. W., & Fahy, J. (2005). The performance impact of marketing resources. Journal of Business Research, 58(1), 18–27.

Hünerberg, R., & Hüttmann, A. (2003). Performance as a basis for price-setting in the cap- ital goods industry:: Concepts and empirical evidence. European Management Journal, 21(6), 717–730.

Hunt, J. M., & Forman, H. (2006). The role of perceived risk in pricing strategy for indus- trial products: A point-of-view perspective. Journal of Product & Brand Management, 15(6), 386–393.

Ingenbleek, P., Debruyne, M., Frambach, R. T., & Verhallen, T. M. M. (2003). Successful new product pricing practices: A contingency approach. Marketing Letters, 14(4), 289–305. Ingenbleek, P., Frambach, R. T., & Verhallen, T. M. (2013). Best practicesfor new product pricing: Impact on market performance and price level under different conditions.

Journal of Product Innovation Management, 30(3), 560–573.

Isaksson, L. E., & Woodside, A. G. (2016). Modeling firm heterogeneity in corporate social performance and financial performance. Journal of Business Research, 69(9), 3285–3314.

ISBM (2012). Insights to action – ISBM B2B marketing trends 2012, Institute for the Study of Business Markets. University Park, PA (USA): Smeal College, Penn State University.

Johnstone, T. (2007). Book cover quote. In J. C. Anderson, N. Kumar, & J. Narus (Eds.), Value merchants: Demonstrating and documenting superior value in business markets. Boston, MA.: Harvard Business School Press.Jones, G. R. (1986). Socialization tactics, self-efficacy, and newcomers’ adjustments to or-ganizations. Academy of Management Journal, 29(2), 262–279.

Kähkönen, M. (2012). Creating long-term value Metso Investor Conference (Metso Capital Day Markets). (Vantaa (Finland)).

Keränen, J., & Jalkala, A. (2013). Towards a framework of customer value assessment in B2B markets: An exploratory study. Industrial Marketing Management, 42(8), 1307–1317.

Kindström, D., Kowalkowski, C., & Nordin, F. (2012). Visualizing the value of service-based offerings: Empirical findings from the manufacturing industry. Journal of Business & Industrial Marketing, 27(7), 538–546.

Koning, P., & Heinrich, C. J. (2013). Cream-skimming, parking and other intended and un- intended effects of high-powered, performance-based contracts. Journal of Policy Analysis and Management, 32(3), 461–483.

Krishnamurthy, C., Johansson, J., & Schlissberg, H. (2003). Solutions selling: Is the pain worth the gain? McKinsey Marketing Solutions.

Kumar, V., Jones, E., Venkatesan, R., & Leone, R. P. (2011). Is market orientation a source of sustainable competitive advantage or simply the cost of competing? Journal of Marketing, 75(1), 16–30.

Lancioni, R. A. (2005). A strategic approach to industrial product pricing: The pricing plan.

Industrial Marketing Management, 34(2), 177–183.

Lancioni, R., Schau, H. J., & Smith, M. F. (2005). Intraorganizational influences on business- to-business pricing strategies: A political economy perspective. Industrial Marketing Management, 34(2), 123–131.

Liozu, S. (2015). Pricing superheroes: How a confident sales team can influence firm per- formance. Industrial Marketing Management, 47, 26–38.

Lussier, B., & Hartmann, N. N. (2017). How psychological resourcefulness increases salesperson’s sales performance and the satisfaction of their customers: Exploring the mediating role of customer-oriented behaviors. Industrial Marketing Management, 59 (in print).

Marketing Science Institute. (2010). 2010–2012 research priorities. In M.S. Institute (Ed.). (Cambridge, MA (USA)).

Marketing Science Institute. (2014). 2014–2016 research priorities. In M.S. Institute (Ed.) (Cambridge, MA (USA)).

Marshall, A. (1925). Letter to A. L. Bowley, 3 March 1901. In A. C. Pigou (Ed.), Memorials of Alfred Marshall (pp. 422). London, UK: Macmillan.

McMurchy, N. (2008). Tough times in IT: How do you exploit the opportunities? Gartner Presentation.

Morgan, N. A., Vorhies, D. W., & Mason, C. H. (2009). Market orientation, marketing capa- bilities, and firm performance. Strategic Management Journal, 30(8), 909–920.

Nagle, T., & Cressman, G. (2002). Don’t just set prices, manage them. Marketing Management, 11(6), 29–33.

Nagle, T., & Holden, R. (2002). The strategy and tactics of pricing: A guide to profitable deci- sion making (3rd ed.). NJ: Prentice Hall Englewood Cliffs.

Nagle, T., Hogan, J., & Zale, J. (2011). The strategy and tactics of pricing: A guide to growing more profitably (5th ed.). Upper Saddle River, NJ: Prentice Hall.

Narver, J. C., & Slater, S. F. (1998). Additional thoughts on the measurement of market ori- entation: A comment on Deshpandè and Farley. Journal of Market-Focused Management, 2(3), 233–236.

Ng, I. C., Ding, D. X., & Yip, N. (2013). Outcome-based contracts as new business model: The role of partnership and value-driven relational assets. Industrial Marketing Management, 42(5), 730–743.

Nunally, J., & Bernstein, I. (1994). Psychometric theory (3rd ed.). New York, NY: McGraw- Hill.

Nunnally, J. (1978). Fundamentals of factor analysis. Psychometric theory (2nd ed.). New York, NY: McGraw-Hill Book Company, 327–404.

Ordanini, A., Parasuraman, A., & Rubera, G. (2013). When the recipe is more important than the ingredients: A qualitative comparative analysis (QCA) of service innovation configurations. Journal of Service Research, 17(2), 134–149.

Pelham, A. M. (2010). The impact of salesperson perception of firm market orientation on behaviors and consulting effectiveness. Journal of Business-to-Business Marketing, 17(2), 105–126.

Periatt, J. A., LeMay, S. A., & Chakrabarty, S. (2004). The selling orientation–customer ori- entation (SOCO) scale: Cross-validation of the revised version. Journal of Personal Selling & Sales Management, 24(1), 49–54.

Piercy, N. F., Cravens, D. W., & Lane, N. (2001). Sales manager behavior control strategy and its consequences: The impact of gender differences. Journal of Personal Selling & Sales Management, 21(1), 39–49.

Piscopo, G., Johnston, W., & Bellenger, D. (2008). Total cost of ownership and customer value in business markets. Advances in Business Marketing and Purchasing, 14, 205–220.

Plank, R. E., & Ferrin, B. G. (2002). How manufacturers value purchase offerings: An ex- ploratory study. Industrial Marketing Management, 31(5), 457–465.

Plouffe, C. R., Williams, B. C., & Wachner, T. (2008). Navigating difficult waters: Publishing trends and scholarship in sales research. Journal of Personal Selling & Sales Management, 28(1), 79–92.

Rackham, N. (1988). SPIN selling. New York, NY: McGraw-Hill.

Richards, K. A., Moncrief, W. C., & Marshall, G. W. (2010). Tracking and updating academic research in selling and sales management: A decade later. Journal of Personal Selling & Sales Management, 30(3), 253–271.

Ridsdale, M. (2011). Steel – Industry background and analysis analyst report. Sydney (Aus- tralia): Resource Capital Research.

Rodriguez, M., & Honeycutt, E. D., Jr. (2011). Customer relationship management (CRM)’s impact on B to B sales professionals’ collaboration and sales performance. Journal of Business-to-Business Marketing, 18(4), 335–356.

Roegner, E., & Gobbi, J. (2001). Effective solutions pricing: How to get the best premium from strategic collaborations McKinsey marketing solutions. McKinsey & Company.

Sackett, P. R., & Larson, J. R. (1990). Research strategies and tactics in industrial and orga- nizational psychology. In M. D. Dunnette, & L. M. Hough (Eds.), Handbook of industrial

and organizational psychology, vol. 1. (pp. 419–489). Palo Alto, CA: Consulting Psy- chologists Press.